Receiving a letter in the mail informing you that your insurance claim has been denied can feel like a punch to the gut. Whether it is a medical bill you thought would be covered, a car repair claim after an accident, or a homeowners insurance claim following property damage, that denial letter represents more than just paperwork. It represents stress, financial worry, and the daunting prospect of navigating a complex appeals process.

Insurance claim denials are far more common than most people realize. According to recent data from the Kaiser Family Foundation, insurers selling plans on HealthCare.gov denied approximately 19% of in-network claims in 2024, with out-of-network claims facing denial rates as high as 37%. These statistics paint a sobering picture of the modern insurance landscape, where nearly one in five claims faces initial rejection.

The good news is that many denied claims can be successfully appealed. Studies have shown that when patients and healthcare providers take the time to appeal denied claims, a significant portion of those denials are overturned. In Medicare Advantage plans, for example, research indicates that approximately 57% of initially denied claims are eventually approved upon appeal.

This article will explore the most common reasons why insurance claims get denied, provide practical guidance on how to appeal a denial, and offer strategies for preventing denials before they happen. By understanding the system and knowing your rights, you can significantly improve your chances of getting the coverage you deserve.

The Scale of the Problem

To truly understand why insurance claims get denied, we must first appreciate the magnitude of the issue. The denial problem is not limited to one type of insurance or one segment of the market. It affects health insurance, auto insurance, homeowners insurance, and virtually every other type of coverage available to consumers.

In the healthcare sector alone, the financial impact is staggering. Hospitals across the United States spend an estimated $19.7 billion annually trying to overturn denied claims. This figure does not include the billions more lost to claims that are never appealed or the administrative costs borne by patients themselves. The cost associated with denied claims increased by 67% in 2022 alone, signaling a systemic breakdown in how claims are prepared and validated.

The denial rates vary significantly depending on the type of insurance and the specific insurer. According to data from the American Hospital Association, commercial payers have initial denial rates of approximately 13.9%, while Medicare Advantage plans average around 15.7%. Some individual insurers report denial rates exceeding 30%, meaning that nearly one-third of all claims submitted to these companies are initially rejected.

What makes these statistics particularly troubling is that many denials are preventable. Industry experts estimate that 60% to 80% of denied claims are overturned when properly appealed, suggesting that a significant portion of initial denials are either incorrect or can be resolved with additional information. This means that millions of Americans are likely paying bills they should not have to pay, simply because they do not know how to navigate the appeals process.

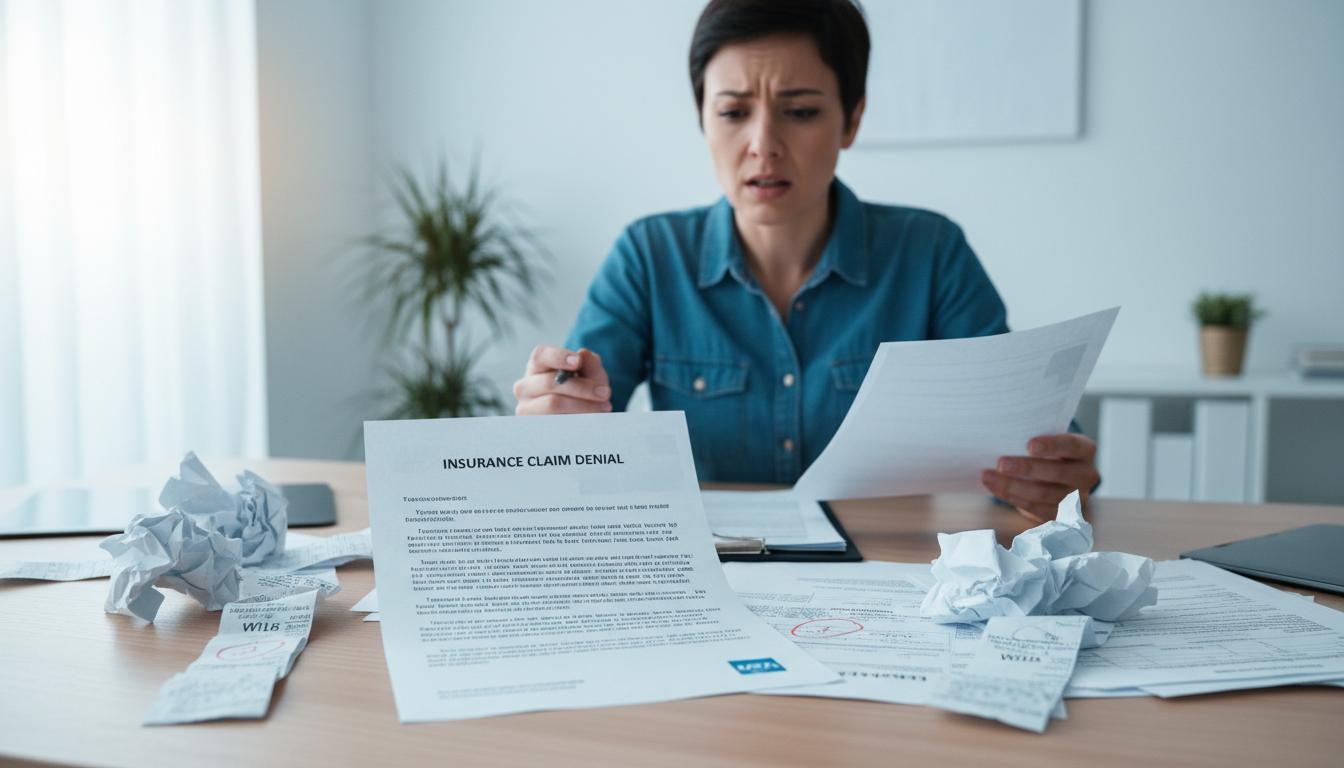

Figure 1: Reviewing an insurance claim denial letter can be overwhelming for many policyholders.

Top Reasons Insurance Claims Get Denied

Insurance claims can be denied for a wide variety of reasons, ranging from simple administrative errors to complex medical necessity determinations. Understanding these reasons is the first step toward preventing denials and successfully appealing them when they occur. Let us examine the most common causes of claim denials in detail.

Administrative and Paperwork Errors

The most common reason for claim denials is also the most frustrating: simple administrative errors. These mistakes can happen at any point in the claims process, from the initial submission to the final review. According to industry data, administrative errors account for approximately 25% of all claim denials, making them the single largest category of preventable denials.

Missing or incorrect patient information is a frequent culprit. Something as simple as a misspelled name, an incorrect date of birth, or a transposed digit in a policy number can result in an automatic denial. These errors often occur during the registration process, when staff members are entering data quickly or dealing with incomplete information from patients.

Coding errors represent another major source of administrative denials. Medical claims rely on complex coding systems, including ICD-10 codes for diagnoses and CPT codes for procedures. When these codes are entered incorrectly, do not match the documentation, or are outdated, the claim will likely be denied. Even experienced billing staff can make coding mistakes, particularly when dealing with unusual procedures or rare conditions.

Duplicate claims are another common administrative issue. Sometimes claims are accidentally submitted twice, or a provider resubmits a claim before the original has been processed. Insurance companies have systems in place to detect duplicate submissions, and these claims are typically denied automatically. While this prevents double payment, it can also cause legitimate resubmissions to be rejected if they are not properly marked.

Timely filing violations represent yet another administrative pitfall. Every insurance plan has deadlines for claim submission, typically ranging from 90 days to one year from the date of service. Claims submitted after these deadlines are generally denied automatically, regardless of their validity. These denials can be particularly heartbreaking for patients who were unaware of the deadline or whose providers failed to submit claims on time.

Coverage and Eligibility Issues

The second major category of denials involves coverage and eligibility problems. These denials occur when the insurance company determines that the service or treatment in question is not covered by the policy, or when the patient was not eligible for coverage at the time the service was provided.

Lapsed coverage is a particularly painful reason for denial. If your insurance policy was not active on the date of service, whether due to non-payment of premiums, a gap between jobs, or any other reason, your claim will almost certainly be denied. This can leave patients facing massive bills for services they believed were covered.

Service exclusions are another common coverage issue. Every insurance policy has a list of services that are explicitly excluded from coverage. These exclusions vary widely between plans and can include everything from cosmetic procedures to experimental treatments to certain types of alternative medicine. Patients are often unaware of these exclusions until they receive a denial letter.

Out-of-network provider denials have become increasingly common as insurance networks have narrowed. When you receive care from a provider who is not in your insurance network, your claim may be denied entirely or paid at a much lower rate. This is particularly problematic in emergency situations, when patients may not have the ability to choose an in-network provider.

Benefit limit denials occur when you have exceeded the maximum amount your insurance plan will pay for a particular service. Many plans have annual or lifetime limits on certain types of care, such as physical therapy visits, mental health sessions, or prescription drug costs. Once these limits are reached, additional claims for the same type of service will be denied.

Medical Necessity Concerns

Medical necessity denials are among the most contentious and complex types of claim denials. These occur when the insurance company determines that a particular treatment, procedure, or service was not medically necessary for the patient’s condition. While medical necessity denials represent only about 5% of all denials according to recent data, they often involve the most expensive and critical treatments.

Insurance companies employ medical directors and review boards to evaluate whether treatments meet their criteria for medical necessity. These criteria are often based on clinical guidelines, peer-reviewed research, and the company’s own internal policies. However, what one physician considers medically necessary may not align with the insurance company’s determination.

Insufficient documentation is a frequent cause of medical necessity denials. When the clinical notes and medical records do not clearly support the need for a particular treatment, the insurance company may deny the claim. This can happen when providers fail to adequately document the patient’s symptoms, previous treatments attempted, or the rationale for choosing a particular approach.

Experimental or investigational treatment denials affect patients seeking cutting-edge or alternative therapies. Insurance companies typically exclude coverage for treatments they consider experimental, meaning they have not yet been proven effective through large-scale clinical trials. This category can include new medications, innovative surgical techniques, and alternative therapies that fall outside mainstream medical practice.

Step therapy requirements can also lead to medical necessity denials. Many insurance plans require patients to try less expensive treatments before approving more costly options. If a provider prescribes a medication or procedure without documenting that the patient first tried and failed the required step therapies, the claim may be denied.

Prior Authorization Problems

Prior authorization has become one of the most significant barriers to insurance coverage in recent years. This process requires providers to obtain approval from the insurance company before performing certain services or prescribing certain medications. Failure to obtain prior authorization when required almost always results in claim denial.

According to recent data, approximately 9% of all claim denials are due to lack of prior authorization. However, this figure varies dramatically by insurer. Some insurance plans report that nearly all of their denials are related to prior authorization issues, while others rarely use this requirement.

The prior authorization process can be incredibly burdensome for both providers and patients. Providers must submit detailed information about the patient’s condition, the proposed treatment, and the medical justification for that treatment. This paperwork can take hours to complete and may require multiple rounds of back-and-forth communication with the insurance company.

Referral requirements are closely related to prior authorization issues. Many insurance plans, particularly HMOs, require patients to obtain a referral from their primary care physician before seeing a specialist. If a patient sees a specialist without the required referral, any claims submitted for that visit will likely be denied.

The rules for prior authorization and referrals vary significantly between insurance plans and can change frequently. What was covered without prior authorization last year may require it this year. Providers who are not up-to-date on the latest requirements may inadvertently submit claims that are destined for denial.

Figure 2: Healthcare providers can be valuable allies in navigating the insurance claims process.

How to Appeal a Denied Claim

Receiving a denial letter is not the end of the road. Every insurance policy includes a process for appealing denied claims, and many denials are successfully overturned through this process. Understanding how to navigate the appeals system can mean the difference between paying a massive bill out of pocket and having your insurance cover the costs as intended.

The first step in any appeal is to understand exactly why your claim was denied. The denial letter you receive from your insurance company must include a specific reason for the denial, as well as information about how to appeal the decision. Take the time to read this letter carefully and make sure you understand the insurer’s rationale.

Gather all relevant documentation before beginning your appeal. This includes the denial letter, your insurance policy documents, all medical records related to the claim, any correspondence with your provider, and any other supporting materials. The more evidence you can provide to support your position, the stronger your appeal will be.

Contact your healthcare provider for assistance. Many providers have staff members who specialize in handling insurance appeals and can provide valuable guidance. Your doctor may also be willing to write a letter of medical necessity explaining why the treatment was appropriate for your condition. This type of professional support can significantly strengthen your appeal.

File your internal appeal within the required timeframe. Most insurance plans give you 180 days from the date of the denial notice to file an internal appeal, but some plans have shorter deadlines. Do not wait until the last minute to begin the process. Submit your appeal as soon as possible to ensure you meet all deadlines.

If your internal appeal is denied, you may have the right to an external review. This process involves having your case reviewed by an independent third party that is not affiliated with your insurance company. External review decisions are binding on the insurance company, meaning they must pay the claim if the external reviewer rules in your favor.

Keep detailed records throughout the appeals process. Document every phone call, including the date, time, and name of the person you spoke with. Save copies of all correspondence and make notes about any verbal communications. This documentation can be invaluable if you need to escalate your appeal or file a complaint with your state insurance department.

Tips for Preventing Claim Denials

While knowing how to appeal a denial is important, preventing denials in the first place is even better. By taking proactive steps before receiving services and staying engaged throughout the claims process, you can significantly reduce your chances of facing a denial.

Verify your coverage before receiving services. Contact your insurance company to confirm that the treatment or procedure you need is covered under your plan. Ask about any prior authorization requirements, referral needs, or other conditions that must be met for the claim to be paid. Getting this information upfront can prevent surprises later.

Choose in-network providers whenever possible. In-network providers have contracts with your insurance company that dictate how much they can charge and how claims are processed. Out-of-network providers do not have these agreements, which often results in higher costs and increased likelihood of claim denials.

Make sure your provider has accurate insurance information. Provide your insurance card at every visit and verify that the information on file is correct. Even small errors in your policy number, group number, or personal information can cause claims to be denied.

Understand your policy’s exclusions and limitations. Read your insurance policy documents carefully to understand what is and is not covered. Pay particular attention to any annual or lifetime limits on specific types of care, as well as any services that are explicitly excluded from coverage.

Follow up on pending claims. Do not assume that no news is good news when it comes to insurance claims. Check the status of your claims regularly and contact your insurance company if a claim has not been processed within a reasonable timeframe. Addressing issues early can prevent them from becoming bigger problems.

Keep copies of everything. Maintain a file with copies of all medical bills, insurance statements, correspondence with your provider and insurance company, and any other relevant documents. Having this information organized and readily available will make it much easier to address any issues that arise.

Consider working with a patient advocate if you are facing a complex situation. Patient advocates are professionals who specialize in helping people navigate the healthcare system and insurance claims process. They can provide valuable guidance and support, particularly for serious or chronic conditions that require extensive medical care.

Insurance claim denials are an unfortunate reality of the modern healthcare and insurance landscape. With denial rates hovering around 20% for many types of insurance, the odds are significant that you or someone you know will face a denied claim at some point. However, understanding why claims get denied and knowing how to respond can make a tremendous difference in the outcome.

The most common reasons for claim denials, administrative errors, coverage issues, medical necessity concerns, and prior authorization problems, are all addressable with the right approach. Many denials can be prevented by taking proactive steps to verify coverage, choose in-network providers, and ensure accurate information is submitted. When denials do occur, a well-prepared appeal has a strong chance of success.

Perhaps most importantly, remember that you are not alone in this process. Healthcare providers, patient advocates, and state insurance departments can all provide assistance and guidance. Your insurance policy grants you specific rights, including the right to appeal denied claims and the right to an external review if your appeal is unsuccessful.

The key takeaways from this article are simple but powerful: understand your insurance coverage, keep detailed records, act quickly when issues arise, and do not be afraid to advocate for yourself. With persistence and the right information, many denied claims can be overturned, ensuring that you receive the benefits you have paid for and deserve.

Insurance is meant to provide peace of mind and financial protection when you need it most. While the claims process can be frustrating and complex, staying informed and engaged will help you navigate the system successfully. The next time you file a claim or receive a denial letter, you will be equipped with the knowledge and strategies needed to achieve the best possible outcome.