Every year, insurance fraud costs Americans more than $308 billion. That is not a typo. It is a staggering sum that affects every single person who pays for insurance, which is just about everyone. When fraudsters cheat the system, honest families foot the bill through higher premiums, stricter policies, and increased scrutiny on legitimate claims.

Insurance fraud is not a victimless crime. It is a sophisticated, organized, and growing problem that spans from staged car accidents to fake injury claims, from arson schemes to elaborate medical billing scams. The people behind these crimes are not always shadowy figures in dark alleys. Sometimes they are your neighbors, your coworkers, or even healthcare professionals you trust.

In this investigative report, we pull back the curtain on the hidden world of insurance fraud. We examine how these schemes work, who is behind them, how investigators catch them, and what the consequences are for both the criminals and the honest policyholders who ultimately pay the price.

The Scale of the Problem

According to the latest data from the Association of British Insurers, fraudulent insurance claims topped 1.16 billion pounds in 2024, representing a 2% increase from the previous year. In the United States, the Coalition Against Insurance Fraud estimates that fraud costs Americans $308.6 billion annually. To put that in perspective, that is more than the entire GDP of countries like Portugal or Chile.

Motor insurance remains the most common target for fraudsters. In the UK alone, insurers detected 51,700 motor scams worth $576 million in 2024. These schemes range from staged accidents at busy intersections to elaborate organized crime rings that orchestrate multiple collisions using damaged vehicles purchased specifically for the purpose.

But car insurance is just the tip of the iceberg. Property insurance fraud, healthcare fraud, workers’ compensation fraud, and life insurance fraud all contribute to the massive financial burden. The FBI estimates that healthcare fraud alone costs the United States tens of billions of dollars each year.

What makes these numbers even more alarming is that they represent only the fraud that gets detected. Industry experts estimate that for every dollar of fraud that is caught, several more slip through undetected. The true cost of insurance fraud may be impossible to calculate precisely, but it is undoubtedly in the hundreds of billions of dollars globally.

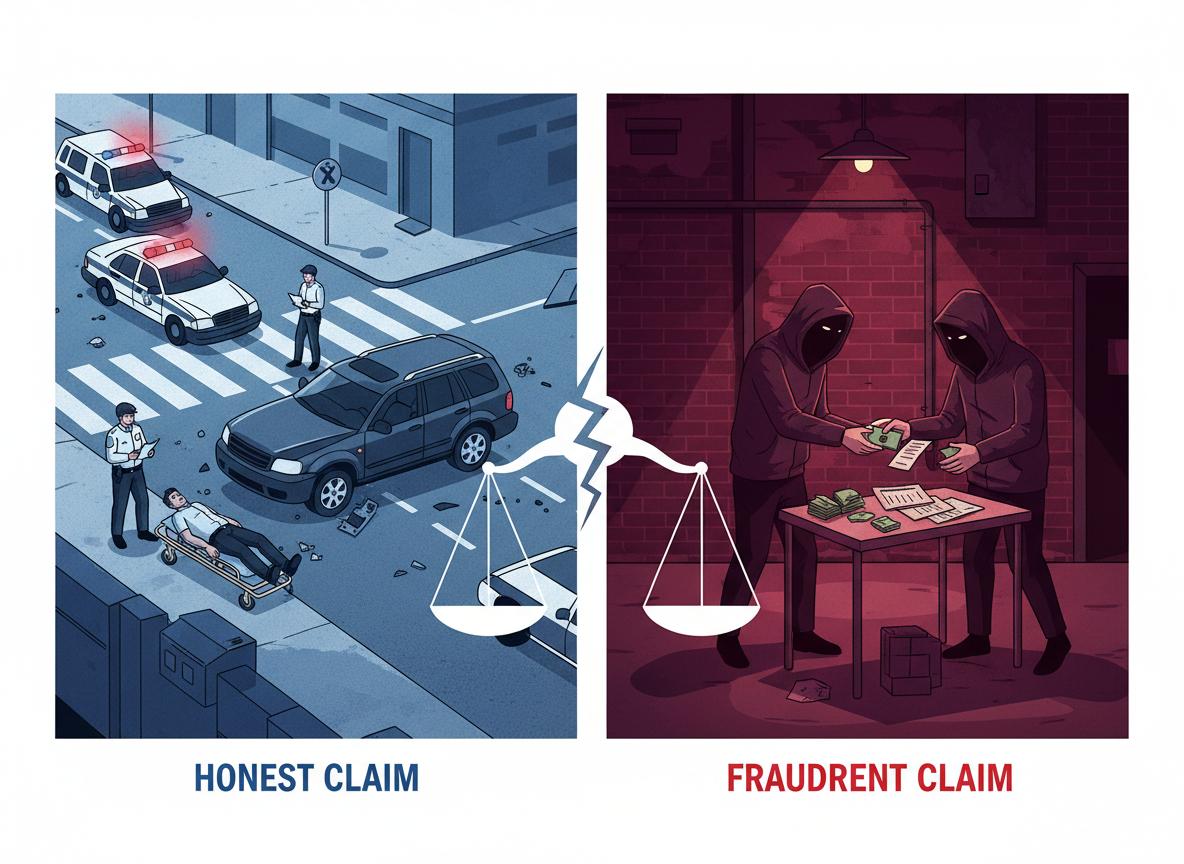

Figure 1: The contrast between honest insurance claims and fraudulent schemes

How the Scams Work

Insurance fraud comes in many forms, but some schemes are more common than others. Understanding how these scams work is the first step in protecting yourself and recognizing when something does not seem right.

Staged

are among the most profitable and widespread schemes. Organized fraud rings in states like California have been known to generate an average of $174,000 through coordinated collisions. These criminals purchase damaged vehicles, stage rear-end collisions at busy intersections, and then file claims for both vehicle damage and fake injuries. The August 2023 case in Santa Clara County involved 23 individuals who used 40 different vehicles over four years to run this exact scam.

Fake injury claims often follow staged accidents. Fraudsters visit multiple doctors to document injuries that never actually occurred. Medical mills, which are clinics set up specifically to generate fraudulent billing, charge insurance companies for unnecessary treatments and examinations. The California Department of Insurance reports that exaggerated soft tissue injuries account for 60% of fraudulent medical claims. These injuries are particularly attractive to fraudsters because they are difficult to disprove medically.

Vehicle arson is another common scheme, particularly for owners of luxury vehicles or those with mechanical problems. When a car needs expensive repairs or when the owner owes more on the loan than the vehicle is worth, some people see arson as a way out. The California Highway Patrol investigates approximately 200 suspected arson cases annually, with conviction rates reaching 85% when proper evidence is collected.

Workers’ compensation fraud is particularly insidious because it exploits systems designed to protect injured workers. Some employees fake injuries that supposedly occurred at work when they were actually injured elsewhere. Others exaggerate the severity of legitimate injuries to extend their time off and collect more benefits. In one notable case, Jeffrey Thranow’s workers’ compensation fraud resulted in over $47,000 in restitution payments to insurance companies.

Life insurance fraud takes many forms as well. Some individuals fake their own deaths to collect benefits, while others take out policies on strangers or distant relatives without their knowledge. There have even been cases of murder disguised as accidents to collect life insurance payouts. These schemes are particularly disturbing because they involve the ultimate betrayal of trust.

Property insurance fraud includes everything from exaggerating the value of stolen items to deliberately setting fire to a home or business. Homeowners facing financial difficulties may see insurance fraud as a way out, destroying their property to collect the payout. Business owners may inflate claims for inventory losses or damage from natural disasters.

The Human Cost

When people think about insurance fraud, they often picture wealthy insurance companies losing money. But the reality is far different. The real victims are everyday people like you and me.

Insurance Commissioner Ricardo Lara confirmed that organized fraud rings drive premium increases statewide. Honest drivers in California pay an estimated $400 annually in additional costs due to fraudulent claims. The National Association of Insurance Commissioners calculates that fraud accounts for 10% of all property and casualty claims, which translates directly into higher rates for every policyholder.

The impact goes beyond just dollars and cents. Legitimate claimants often face increased scrutiny and longer processing times as insurance companies implement stricter verification procedures to combat fraud. Someone who has genuinely been injured in a car accident may find themselves under investigation, asked to provide extensive documentation, and forced to wait longer for the benefits they desperately need.

There is also a societal cost. When healthcare providers engage in fraud, they drive up medical costs for everyone. When workers’ compensation fraud is rampant, businesses face higher premiums that can affect their ability to hire and expand. The ripple effects of insurance fraud touch every corner of the economy.

Small businesses are particularly vulnerable to the effects of insurance fraud. Unlike large corporations that can absorb higher premiums, small businesses often operate on thin margins. When their insurance costs increase due to fraud in the system, they may be forced to cut employee hours, delay expansion plans, or even close their doors permanently.

The elderly are another vulnerable population. Seniors on fixed incomes face the same premium increases as everyone else, but they have less ability to absorb the additional costs. Some seniors may even be tempted to commit fraud themselves, exaggerating claims to make ends meet, which only perpetuates the cycle of rising costs.

The Fight Back: Detection and Investigation

Insurance companies are not sitting idle while fraudsters drain billions from the system. They have developed sophisticated methods to detect and investigate suspicious claims, combining traditional investigative techniques with cutting-edge technology.

The investigation process typically begins when a claim is flagged as suspicious. This can happen through automated systems that analyze claim patterns, through tips from whistleblowers, or through the intuition of experienced claims adjusters who notice something does not add up.

Once a claim is flagged, investigators begin gathering evidence. This includes collecting and reviewing documents like medical records, police reports, and repair estimates. They conduct interviews with claimants, witnesses, and service providers. They may perform on-site surveys of accident locations or damaged properties. In some cases, they conduct surveillance to verify whether claimed injuries are genuine.

Technology has revolutionized fraud detection. Modern insurers use data analytics to identify unusual patterns that might indicate fraud. Machine learning algorithms can analyze thousands of claims in seconds, flagging suspicious cases for further investigation. Social network analysis helps identify connections between fraud rings and suspicious entities. Predictive modeling uses historical data to predict the likelihood that a new claim might be fraudulent.

Insurance companies also collaborate with law enforcement agencies, sharing information about suspected fraud and working together on investigations. Many states have dedicated insurance fraud bureaus that specialize in prosecuting these crimes.

The role of artificial intelligence in fraud detection cannot be overstated. Modern AI systems can analyze vast amounts of data in real-time, identifying patterns that would be impossible for human investigators to spot. These systems learn from each case they process, continuously improving their ability to detect suspicious activity.

Social media has become a valuable tool for investigators as well. Fraudsters who claim to be severely injured may post photos of themselves engaging in physical activities on social media platforms. Investigators can use this publicly available information to verify or disprove injury claims. A person claiming disability benefits who posts photos of themselves hiking or playing sports is creating evidence against themselves.

Data sharing between insurance companies has also improved detection rates. When a person files multiple claims with different insurers, cross-referencing databases can reveal suspicious patterns. Someone who has filed several similar claims with different companies over a short period may be running a fraud scheme.

Consequences for Fraudsters

The penalties for insurance fraud can be severe, and prosecutors are increasingly aggressive in pursuing these cases. Depending on the size of the fraudulent claim and the state where it occurred, insurance fraud can be charged as either a misdemeanor or a felony.

Criminal penalties can include jail time ranging from a few months to several decades in prison. Fines can reach $100,000 or more. Courts routinely order restitution payments that require fraudsters to repay the money they stole, often with additional penalties on top. A $25,000 fraudulent claim can result in $50,000 or more in total penalties.

The August 2023 organized fraud ring case in Santa Clara County illustrates how serious these consequences can be. Twenty-three individuals faced felony charges for a four-year fraud operation. Each defendant faced potential sentences of up to five years in prison and fines reaching $50,000. The California Department of Insurance reports that criminal convictions for insurance fraud have increased by 23% over the past three years, reflecting stronger enforcement efforts.

Beyond criminal penalties, fraudsters face other consequences. A criminal conviction creates a permanent record that can affect employment opportunities, professional licenses, and future insurance coverage. Someone convicted of insurance fraud may find it difficult or impossible to obtain insurance in the future, or may be forced to pay extremely high premiums.

Protecting Yourself

While the fight against insurance fraud is largely waged by insurance companies and law enforcement, there are steps that ordinary people can take to protect themselves and help combat this problem.

First, be vigilant after any accident. If you are involved in a collision, document everything. Take photos of the scene, the vehicles involved, and any visible damage. Get contact information from witnesses. File a police report, even for minor accidents. This documentation can protect you if someone later tries to exaggerate their claim.

Be wary of strangers who approach you after an accident offering to connect you with lawyers, doctors, or auto repair shops. These could be runners working for fraud rings. Stick with service providers you know and trust, or ask your insurance company for recommendations.

Review your insurance statements carefully. Look for any services or treatments that you do not recognize. If you spot something suspicious, contact your insurance company immediately. Many insurers have fraud hotlines where you can report suspicious activity anonymously.

Finally, resist the temptation to exaggerate legitimate claims. Soft fraud, such as inflating the value of stolen items or exaggerating the extent of damage, may seem harmless, but it contributes to the overall problem of insurance fraud and can result in serious consequences if discovered.

Insurance fraud is a hidden epidemic that costs honest families billions of dollars each year. From staged accidents to fake injury claims, from organized crime rings to individual opportunists, fraudsters are constantly finding new ways to exploit the insurance system.

The good news is that insurance companies, law enforcement agencies, and prosecutors are fighting back with increasingly sophisticated detection methods and aggressive prosecution. The bad news is that the problem continues to grow, and honest policyholders continue to pay the price through higher premiums and increased scrutiny.

Combating insurance fraud requires vigilance from everyone involved in the system. Insurance companies must continue to invest in detection technology. Law enforcement must remain committed to investigating and prosecuting these crimes. And ordinary citizens must stay alert, document carefully, and resist the temptation to pad their own claims.

Education plays a crucial role in prevention. Many people do not realize that even small acts of fraud, like exaggerating the value of a stolen item or claiming old damage was caused by a recent storm, contribute to the larger problem. Public awareness campaigns can help people understand that insurance fraud is not a victimless crime and that the consequences affect everyone.

Technology will continue to evolve in the fight against fraud. As fraudsters develop new schemes, detection systems must adapt to catch them. The arms race between criminals and investigators shows no signs of slowing down. Investment in advanced analytics, artificial intelligence, and data sharing platforms will be essential to staying ahead of sophisticated fraud operations.

Legislation also plays an important role. Stronger penalties for insurance fraud can serve as a deterrent, while better funding for insurance fraud bureaus can improve enforcement. Some states have implemented mandatory reporting requirements that help identify patterns of fraud across multiple jurisdictions.

The insurance industry itself must continue to balance fraud prevention with customer service. While it is important to catch fraudsters, legitimate claimants should not be made to feel like criminals. The goal is to create a system that efficiently processes honest claims while effectively identifying and stopping fraudulent ones.

The next time you pay your insurance premium and wonder why it seems so high, remember that a portion of that cost is the hidden tax of insurance fraud. It is a problem that affects us all, and it will take all of us working together to solve it. By staying informed, remaining vigilant, and committing to honesty in our own dealings with insurance companies, we can all play a part in reducing this costly epidemic.

As consumers, we have more power than we realize. By reporting suspicious activity, refusing to participate in fraudulent schemes, and supporting stronger enforcement measures, we can help create an insurance system that works fairly for everyone. The fight against insurance fraud is ultimately a fight for fairness, honesty, and the integrity of the systems we all depend on.