India’s insurance sector has grown significantly over the past decade, with the life insurance sector recording a compound annual growth rate of over 11% and the general insurance sector achieving even higher growth rates. Yet, beneath these impressive numbers lies a troubling truth: rural India, home to nearly 65% of the country’s population, remains largely outside the protective umbrella of insurance coverage.

According to recent data from the Insurance Regulatory and Development Authority of India (IRDAI), India’s total insurance penetration has remained stagnant at just 3.7% of GDP – far below the global average. While urban India has seen increasing adoption of various insurance products, rural areas continue to struggle with abysmally low coverage rates that leave millions vulnerable to financial shocks.

The numbers paint a concerning picture. Only about half of India’s rural population has access to government health insurance schemes. More alarmingly, over 61% of rural residents have no life insurance coverage whatsoever, leaving their families exposed to severe financial hardship in the event of an unexpected death. Over 34% of rural residents lack any form of government health insurance, forcing them to either skip medical treatment or fall into debt when health emergencies strike.

Understanding the Insurance Awareness Gap

One of the most significant barriers to insurance penetration in rural India is the profound lack of awareness and financial literacy. According to the National Council of Applied Economic Research (NCAER), only 23% of Indian adults demonstrate a basic understanding of insurance concepts such as premiums, sum assured, policy tenure, and exclusions. In rural and semi-urban areas, this figure drops to below 15%, despite these regions being more vulnerable to health emergencies, agricultural losses, and climate-related disasters.

For many rural residents, the concept of insurance remains abstract and difficult to grasp. Unlike tangible products that provide immediate benefits, insurance offers protection against future uncertainties – a value proposition that is hard to appreciate when daily survival is itself a challenge. When a farmer earns between Rs. 8,000 to Rs. 10,000 per month, setting aside money for an intangible product with deferred benefits seems like a luxury they cannot afford.

“Insurance is something we hear about on television, but it doesn’t feel real to us. We work hard every day, and when money is tight, we think about food, seeds, and medicine – not about what might happen tomorrow.” – Ramesh Yadav, small farmer from Uttar Pradesh

This sentiment is echoed across rural India, where the immediate needs of survival consistently outweigh the abstract promise of future protection. The lack of structured financial education in schools and workplaces, combined with limited access to unbiased advisory services, has created a knowledge gap that insurance companies have struggled to bridge.

The Accessibility Challenge: When Insurance Offices Are Miles Away

Even when rural residents understand the importance of insurance, accessing it remains a significant hurdle. India’s insurance distribution model remains heavily dependent on physical intermediaries such as agents, corporate agents, and brokers. However, over 92% of these agents are concentrated in Tier 1 and Tier 2 cities, creating a severe urban-centric distribution bias.

Less than 20% of Indian villages have access to any formal insurance channel, despite being home to nearly two-thirds of the population. For a farmer living in a remote village, the nearest insurance office might be hours away, requiring multiple bus journeys and lost wages. This geographical barrier effectively excludes millions from even considering insurance as an option.

The concentration of insurance infrastructure in urban areas reflects a broader market failure. Insurance companies, driven by profitability concerns, have historically focused on urban customers who offer higher premium potential and lower distribution costs. Rural markets, with their low-ticket-size policies and high servicing costs, have been largely ignored.

The Affordability Conundrum: When Premiums Feel Like a Burden

Economic constraints severely limit the affordability of insurance in low-income segments. With average monthly rural household incomes ranging between Rs. 8,000 and Rs. 10,000, even a modest annual health or term life premium becomes a significant financial burden. For families living on the edge of subsistence, every rupee counts, and insurance premiums often feel like an expense they simply cannot justify.

“When my daughter fell ill last year, I had to borrow Rs. 20,000 from the moneylender at 24% interest. If I had spent money on insurance premiums earlier, I wouldn’t have had to take that loan. But at that time, putting food on the table seemed more important than paying for something I might never use.” – Sunita Devi, daily wage laborer from Bihar

This dilemma is central to the affordability challenge. Insurance products are often designed with urban consumers in mind, failing to address the unique risk profiles, income patterns, and preferences of rural households. The mismatch between product design and customer reality results in poor adoption and even poorer renewal rates.

The Trust Deficit: When Promises Are Broken

Trust in the insurance system is heavily influenced by the transparency and timeliness of claims settlement. Unfortunately, this is where the Indian insurance sector has often fallen short, particularly in rural areas where stories of delayed or denied claims spread quickly through communities.

The life insurance sector maintains relatively high claim settlement ratios, with LIC at 98.7% and private insurers averaging 96.4%. However, delays, documentation burdens, and claim repudiations remain common grievances. In the general insurance sector, the claim repudiation ratio hovers around 6.5%, with higher figures in motor and health insurance – often due to misrepresentation, non-disclosure, or inadequate documentation.

The PMFBY scheme, despite its ambitious goals, has been plagued by implementation challenges. Between 2016 and 2023, insurers collected Rs. 1,97,657 crore in premiums (including subsidies) but paid out only Rs. 1,40,038 crore in claims. More troublingly, of the 56.80 crore farmers enrolled, only 23.22 crore received claim settlements. Stories of farmers receiving absurdly low compensation – such as the Maharashtra farmer who got just Rs. 2.30 for his destroyed crop despite paying Rs. 1,500 in premiums – have eroded trust in the entire system.

Crop Insurance: A Case Study in Rural Insurance Challenges

The Pradhan Mantri Fasal Bima Yojana (PMFBY), launched in 2016 with much fanfare, illustrates the multifaceted challenges of rural insurance. Designed to provide comprehensive financial security to farmers who lose crops due to natural calamities, the scheme has struggled to achieve its objectives.

One major issue is the area-based approach to loss assessment. Rather than evaluating individual farm losses, the scheme relies on satellite imagery and crop-cutting experiments at the village or block level. This methodology often fails to capture the reality on the ground, leading to situations where farmers with significant losses receive minimal or no compensation.

The problem of adverse selection has also plagued the scheme. After enrollment was made voluntary in 2020, only farmers with high-risk land – those most prone to floods or droughts – chose to participate. This skew toward high-risk cultivators has driven up premiums, creating a cycle where the scheme becomes increasingly expensive to sustain.

Several states, including Bihar, Jharkhand, and West Bengal, have opted out of PMFBY, citing fiscal unsustainability. The absence of strong accountability mechanisms or penalty-based settlement ratios creates an incentive within the system to limit payouts, further undermining farmer confidence.

Health Insurance: The Ayushman Bharat Challenge

Ayushman Bharat-Pradhan Mantri Jan Arogya Yojana (PM-JAY), the world’s largest publicly financed health insurance program, has also faced significant implementation challenges in rural areas. Despite being enrolled, studies show that only 48.4% of beneficiaries in some regions actually access PM-JAY services.

The most significant barriers include inadequate road infrastructure, limited awareness of empanelled hospitals, and gaps in health literacy. Administrative and financial obstacles, while often mentioned, are surprisingly not the primary deterrents. Instead, the inability to navigate the healthcare system and lack of information about scheme entitlements prevent many rural residents from utilizing their coverage.

Additionally, over 21% of the rural population lacks access to a commutable chemist store, and only around 12% can access government medical stores like Pradhan Mantri Jan Aushadhi Kendra. This infrastructure gap means that even those with health insurance struggle to obtain the medicines they need.

The Gender Dimension: Women and Insurance

The insurance gap in rural India has a significant gender dimension. In many rural households, financial decisions are predominantly made by men, leaving women with limited autonomy over choices related to insurance participation. Research indicates that 60% of rural women report that financial decisions in their households are made by male family members, with only 20% having full control over such decisions.

This gender bias leads to lower insurance penetration among women, particularly those with limited education or from marginalized communities. Women may not actively engage in discussions about financial products, creating a barrier to insurance uptake that is often overlooked in policy design.

Furthermore, 40% of rural women surveyed in various studies were found to be illiterate, and only 10% had completed higher secondary education. This educational gap compounds the awareness and accessibility challenges, making it even harder for women to understand and access insurance products.

Microinsurance: A Ray of Hope?

Microinsurance has emerged as a potential solution for extending insurance coverage to rural India. These products, designed specifically for low-income households, offer basic protection against common risks such as death, illness, crop loss, livestock mortality, and accidents at minimal premiums.

The microinsurance market in India reached USD 428.4 million in 2024 and is projected to expand to USD 1,693.3 million by 2033. Government initiatives like Pradhan Mantri Jan Dhan Yojana (PMJDY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY) have contributed to this growth, alongside technological innovations in digital distribution and mobile claims processing.

However, microinsurance faces its own set of challenges. Low awareness, affordability barriers, and distribution gaps in rural areas continue to limit its reach. The overlap between social insurance schemes and microinsurance products creates confusion in the market, while high delivery costs make microinsurance unviable for many insurers.

The Path Forward: What Needs to Change

Addressing the insurance gap in rural India requires a multi-pronged approach that tackles awareness, accessibility, affordability, and trust simultaneously.

Financial Literacy and Awareness: Structured financial education programs targeting rural populations are essential. These programs should demystify insurance concepts, explain the claims process, and build understanding of how insurance can protect against financial shocks. Leveraging local media, community leaders, and self-help groups can help spread awareness effectively.

Distribution Innovation: Expanding the network of banking correspondents, Common Service Centres (CSCs), and microfinance institutions can improve last-mile delivery of insurance services. Digital enrollment and Aadhaar-based onboarding have shown promise in simplifying policy enrollment and reducing paperwork.

Product Design: Insurance products need to be redesigned with rural customers in mind. This means flexible premium payment options that align with seasonal income patterns, simplified documentation requirements, and coverage that addresses the specific risks faced by rural households.

Claims Process Reform: Timely and transparent claim settlements are crucial for building trust. Technology solutions such as satellite-based crop assessment, mobile claims processing, and direct benefit transfers can reduce delays and improve the customer experience.

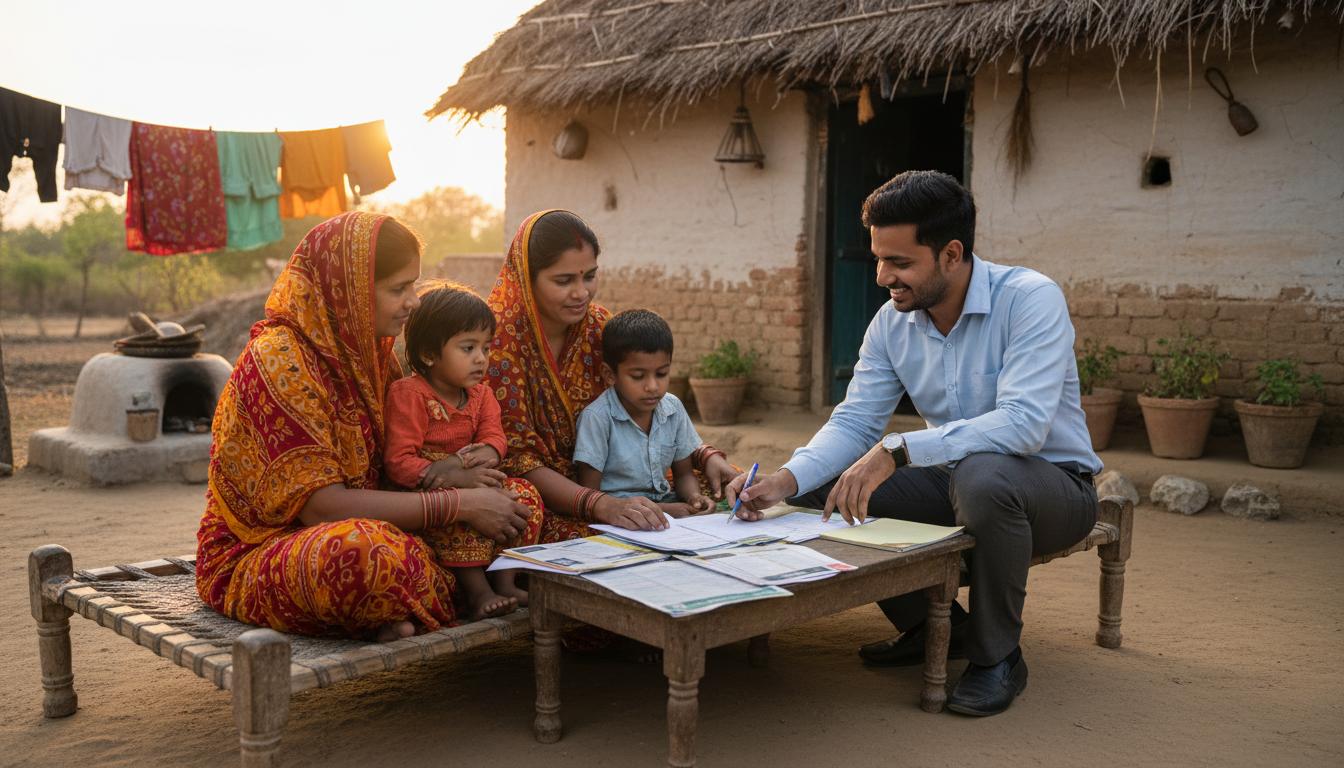

A rural family engages with an insurance agent to understand coverage options – bridging the awareness gap is crucial for expanding insurance penetration in rural India.

Bridging the Divide

The insurance gap in rural India is not just a financial services problem – it is a development challenge with profound implications for poverty reduction, health outcomes, and economic resilience. When a farmer loses his crop to drought, when a laborer cannot afford hospitalization, when a family loses its breadwinner without any financial cushion – the absence of insurance deepens poverty and perpetuates inequality.

India’s insurance sector has the products, the technology, and the regulatory framework to extend coverage to rural areas. What is needed now is the will to redesign business models, invest in distribution infrastructure, and prioritize customer trust over short-term profitability.

For millions of rural Indians, insurance remains an abstract concept, an urban luxury, or a broken promise. Changing this reality will require sustained effort from insurers, policymakers, civil society, and communities themselves. Only then can the protective umbrella of insurance truly cover all of India, not just its cities.