Insurance, at its core, is a simple yet profound concept. It is the promise of protection, a safety net that catches us when life takes an unexpected turn. It is the collective pooling of resources to help those in need, a practice that has existed in various forms across human civilizations for thousands of years. In India, the story of insurance is not merely a tale of financial products and corporate entities. It is a narrative woven into the very fabric of Indian society, reflecting the nation’s economic aspirations, social values, and technological progress.

The evolution of insurance in India is a fascinating journey that spans over two centuries. From the ancient concepts of mutual aid embedded in Indian philosophy to the sophisticated digital insurance platforms of today, this journey mirrors India’s transformation from a colonial economy to one of the world’s fastest-growing major economies. Understanding this evolution is not just about appreciating historical milestones. It is about recognizing how financial protection has become an essential pillar of economic security for millions of Indian families.

This comprehensive exploration will take you through the various phases of insurance development in India. We will examine how the sector emerged during the colonial era, how it was reshaped through nationalization, how liberalization opened new doors, and how digital technology is revolutionizing the industry today. Along the way, we will encounter the key institutions, regulatory frameworks, and visionary policies that have shaped the Indian insurance landscape.

Ancient Foundations: The Philosophical Roots of Risk Sharing

Long before the formal insurance industry took shape in India, the subcontinent had developed sophisticated concepts of mutual aid and collective risk-sharing. Ancient Indian texts reveal that the principles underlying modern insurance were not foreign imports but had indigenous roots in Indian philosophy and social organization.

The writings of Manu in the Manusmriti, Kautilya in the Arthashastra, and Yagnavalkya in the Dharmasastra all contain references to pooling resources that could be redistributed during times of calamity. These ancient scholars recognized that communities needed mechanisms to support members affected by epidemics, floods, fires, and famines. The concept of mutual assistance was deeply embedded in the Indian social fabric, with communities coming together to help those who suffered losses.

Marine trade loans and carriers’ contracts in ancient India also displayed early insurance-like characteristics. Merchants engaged in overseas trade would enter into agreements where lenders would forgive loans if ships were lost at sea, in exchange for higher interest rates. These arrangements spread risk between lenders and borrowers, functioning similarly to modern marine insurance.

The joint family system prevalent in India also served as an informal insurance mechanism. The extended family provided financial support to members facing hardships, whether through death, illness, or property loss. While not formal insurance in the modern sense, these social structures fulfilled similar protective functions.

Understanding these ancient foundations is important because it demonstrates that the concept of financial protection is not alien to Indian culture. When modern insurance was introduced to India, it found fertile ground in a society that already valued collective security and mutual assistance.

The Colonial Era: Birth of Modern Insurance in India (1818-1947)

The modern insurance industry in India began with the arrival of British colonial powers. The first life insurance company on Indian soil was established in 1818 when the Oriental Life Insurance Company opened its doors in Calcutta. However, this company primarily served European residents and explicitly excluded Indian lives from coverage. The premiums were high, and the benefits were reserved for the colonial elite.

The Oriental Life Insurance Company eventually failed in 1834, but it had set a precedent. In 1829, the Madras Equitable began transacting life insurance business in the Madras Presidency, marking another step in the industry’s early development. These initial ventures were followed by the enactment of the British Insurance Act in 1870, which provided a regulatory framework for insurance operations.

The late nineteenth century witnessed the emergence of Indian-owned insurance companies. The Bombay Mutual Life Assurance Society, established in 1871, was the first Indian life insurance company to provide coverage to Indian lives at reasonable rates. This was followed by the Oriental Life Assurance Company in 1874 and the Empire of India Life Assurance Company in 1897. These companies were established in the Bombay Presidency and represented the growing entrepreneurial spirit among Indian businessmen.

The period was still dominated by foreign insurance offices such as Albert Life Assurance, Liverpool and London Globe Insurance, and Royal Insurance. These foreign companies gave stiff competition to Indian enterprises but also helped spread awareness about insurance concepts among the Indian population.

The early twentieth century saw a mushrooming growth of insurance companies, particularly during the Swadeshi movement that encouraged Indians to support indigenous businesses and boycott British goods. From just 44 companies with total business-in-force of Rs. 22.44 crore, the number grew to 176 companies with business-in-force of Rs. 298 crore by 1938. This rapid growth, while demonstrating increasing awareness about insurance, also led to problems. Many financially unsound companies were floated, and allegations of unfair trade practices became common.

Early Regulation and Legislative Framework

The need for regulation became apparent as the insurance sector expanded. The Indian Life Assurance Companies Act of 1912 was the first statutory measure to regulate life insurance business in India. This act required insurance companies to publish their returns and maintain certain standards of financial soundness. In 1914, the Government of India began publishing the returns of insurance companies, bringing greater transparency to the sector.

The Indian Insurance Companies Act was enacted in 1928 to enable the government to collect statistical information about both life and non-life insurance businesses. This act covered Indian and foreign insurers as well as provident insurance societies, giving the government better oversight of the industry.

A significant milestone came in 1938 when the Insurance Act was passed, consolidating and amending earlier legislation. This comprehensive act was designed to protect the interests of the insuring public and provided for uniform government control over all insurers. The Insurance Act of 1938 remains the foundational legislation governing insurance in India to this day, though it has been amended numerous times.

The Insurance Amendment Act of 1950 abolished Principal Agencies, which had been a source of concern due to potential conflicts of interest. This amendment also made other far-reaching changes to make insurance institutions more useful for the country’s economic growth. The Ranganathan Committee, which reviewed the entire insurance law, provided the basis for these amendments.

General Insurance: Parallel Development

While life insurance was developing rapidly, general insurance also found its footing in India. The roots of general insurance can be traced to the establishment of the Triton Insurance Company Limited in 1850 in Calcutta by the British. This was the first general insurance company in India.

In 1907, the Indian Mercantile Insurance Limited was established, becoming the first company to transact all classes of general insurance business. This was a significant development as it demonstrated that Indian companies could compete in the general insurance sector as well.

The General Insurance Council was formed in 1957 as a wing of the Insurance Association of India. The council framed a code of conduct to ensure fair conduct and sound business practices in the industry. The Insurance Act was amended in 1968 to regulate investments and set minimum solvency margins, strengthening the financial stability of general insurance companies.

Post-Independence Nationalization: A New Era Begins (1950-1990)

The period following India’s independence in 1947 marked a significant transformation in the insurance sector. The new government, committed to socialist principles and state-led development, viewed insurance as a crucial instrument for mobilizing savings and providing financial security to the masses.

The demand for nationalization of the life insurance industry had been growing since the 1940s. The government believed that a state-owned insurance corporation would be better positioned to spread insurance to rural areas, protect policyholders from mismanagement, and channel insurance funds into nation-building activities. On January 19, 1956, the Government of India issued an ordinance to nationalize the life insurance sector. This was followed by the Life Insurance Corporation Act, which was passed by Parliament on June 19, 1956.

The Life Insurance Corporation of India (LIC) was formally created on September 1, 1956, with a capital contribution of Rs. 5 crore from the Government of India. The new corporation absorbed 154 Indian insurance companies, 16 non-Indian companies, and 75 provident societies, totaling 245 insurers. This massive consolidation created a single, state-owned entity that would dominate Indian life insurance for the next four decades.

The objectives of LIC were clearly defined. The corporation was tasked with spreading life insurance widely across the country, particularly in rural areas. It was to reach all insurable persons in the country, providing them adequate financial cover at reasonable cost. LIC was also expected to invest its funds in ways that would support the government’s development plans while ensuring the safety and security of policyholders’ money.

LIC’s formation represented a bold experiment in using insurance as a tool for social and economic development. The corporation established an extensive network of offices across the country, including in remote rural areas where no private insurer had ventured. It developed products suited to the needs of different segments of society, from wealthy urban professionals to poor farmers in villages.

The success of life insurance nationalization led to similar action in the general insurance sector. The General Insurance Business (Nationalization) Act was passed in 1972, and the General Insurance Corporation of India (GIC) was incorporated as a company in 1971. On January 1, 1973, the general insurance business was nationalized, with GIC taking over the operations of existing general insurance companies.

GIC was established with four subsidiaries: National Insurance Company, New India Assurance Company, Oriental Insurance Company, and United India Insurance Company. These subsidiaries operated in different regions of the country, though they eventually began competing with each other as well. GIC itself functioned as the national reinsurer, providing reinsurance support to the subsidiaries and other Indian insurers.

The Nationalization Era: Achievements and Challenges

The nationalization era brought both significant achievements and notable challenges to the Indian insurance sector. On the positive side, insurance penetration increased substantially as LIC and GIC expanded their reach to previously underserved areas. The number of insurance agents grew exponentially, creating employment opportunities while spreading insurance awareness. Insurance funds became an important source of long-term capital for government projects and infrastructure development.

LIC, in particular, became a household name in India. It developed innovative products like the Money Back policy, which combined insurance protection with periodic returns, making it attractive to Indian savers. The corporation’s agents became ubiquitous, present in virtually every town and village across the country. By the early 1990s, LIC had issued millions of policies and had become one of the largest life insurance companies in the world by number of policies.

However, the monopoly structure also created problems. Without competition, there was little incentive for product innovation or service improvement. Customer service often suffered, with long delays in policy issuance and claims settlement. The sector became bureaucratic and slow to adapt to changing customer needs. Insurance penetration, while improved, remained low compared to international standards.

The closed nature of the sector also meant that Indian insurance remained isolated from global developments. International best practices in underwriting, risk management, and customer service were slow to reach India. The sector was in need of reform, and the economic liberalization of the 1990s would provide the catalyst for change.

The Road to Liberalization: The Malhotra Committee (1991-1999)

The economic reforms initiated in 1991, which transformed many sectors of the Indian economy, eventually reached the insurance sector as well. In 1993, the Government of India set up a committee under the chairmanship of R. N. Malhotra, former Governor of the Reserve Bank of India, to propose recommendations for reforming the insurance sector.

The Malhotra Committee was tasked with examining the structure of the insurance industry and recommending changes that would complement the broader financial sector reforms. The committee studied insurance sectors in various countries, consulted with stakeholders, and examined the specific conditions of the Indian market.

The committee submitted its report in 1994, and its recommendations were far-reaching. The most significant recommendation was that the private sector should be permitted to enter the insurance industry. The committee argued that competition would lead to better products, improved service, and greater insurance penetration. It also recommended that foreign companies be allowed to enter the Indian market, preferably through joint ventures with Indian partners.

Other important recommendations included the establishment of an independent regulatory body for the insurance sector, reduction in the government’s stake in insurance companies, and greater flexibility in investment norms. The committee also suggested measures to protect policyholders’ interests and ensure the financial soundness of insurance companies.

The recommendations of the Malhotra Committee sparked intense debate. Supporters argued that liberalization would bring much-needed competition and innovation to the sector. Opponents expressed concerns about foreign dominance and the potential impact on LIC and GIC. After several years of discussion and deliberation, the government decided to move forward with reform.

IRDAI: The Guardian of Indian Insurance (1999-Present)

The Insurance Regulatory and Development Authority (IRDA) was established as an autonomous body under the IRDA Act of 1999. The authority was later renamed the Insurance Regulatory and Development Authority of India (IRDAI) in 2015 to emphasize its national role. IRDAI was conferred with statutory status and began operations as the principal regulator of the Indian insurance sector in 2000.

IRDAI’s mission was clear: to protect the interests of policyholders, regulate the insurance industry, promote its orderly growth, and ensure the financial stability of insurance companies. The authority was given comprehensive powers to frame regulations, grant licenses to insurance companies, monitor their operations, and take enforcement action when necessary.

The establishment of IRDAI marked a watershed moment in Indian insurance history. For the first time, there was a dedicated regulatory body focused solely on the insurance sector. IRDAI set about creating a comprehensive regulatory framework that would govern all aspects of insurance operations, from company formation to product approval, from sales practices to claims settlement.

In August 2000, IRDAI opened the insurance market to private players by inviting applications for registration. This ended the monopoly of government-owned insurance companies and ushered in a new era of competition. Foreign companies were allowed to participate in Indian joint ventures with ownership of up to 26 percent, a limit that has since been increased to 74 percent.

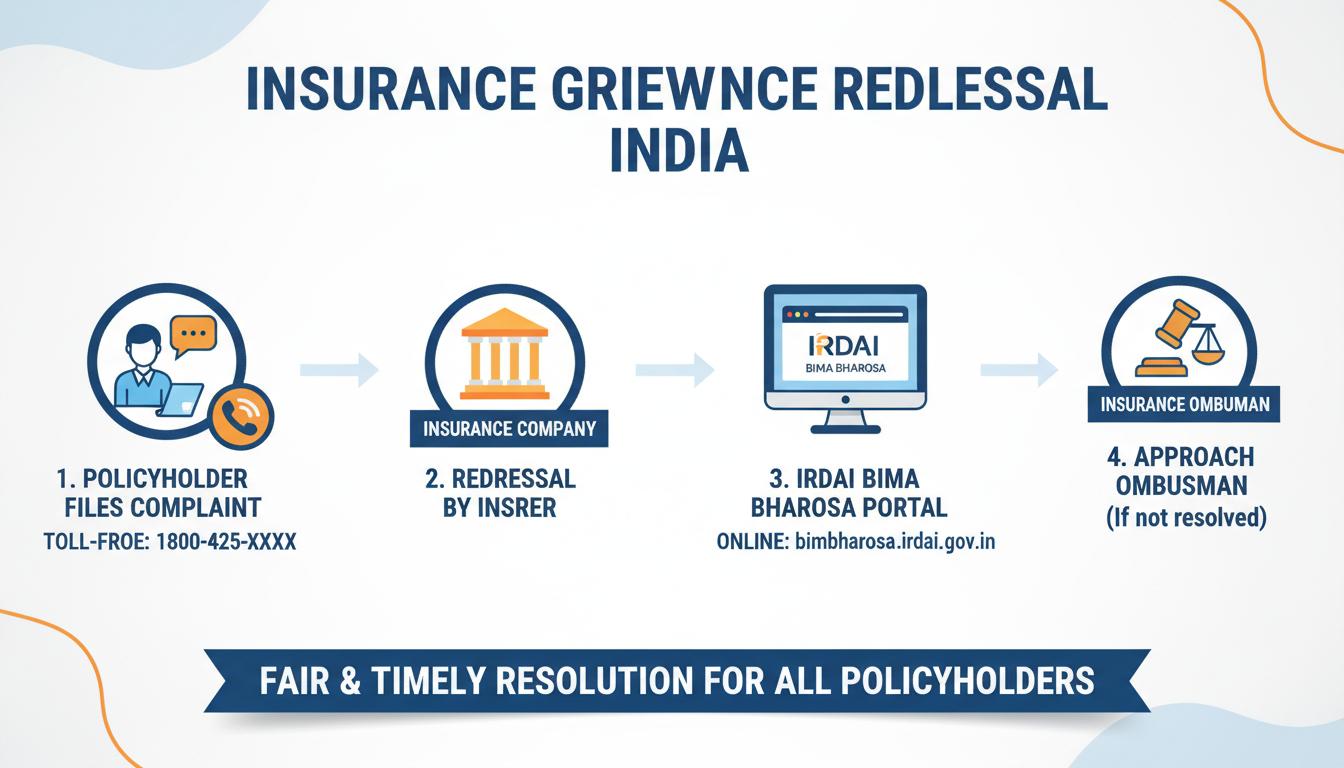

IRDAI’s regulatory framework covered numerous areas. It established capital requirements for insurance companies to ensure their financial soundness. It created guidelines for product design and pricing to protect policyholders. It regulated insurance intermediaries such as agents and brokers to ensure fair sales practices. It mandated disclosures to ensure transparency. It established grievance redressal mechanisms to protect consumer interests.

The authority also played a proactive role in promoting insurance awareness and penetration. It launched various initiatives to educate the public about insurance and encouraged insurers to develop products for underserved segments. IRDAI’s regulatory sandbox allowed insurers to test innovative products and services in a controlled environment, fostering innovation while managing risk.

The Private Insurance Boom: Competition and Innovation (2000-2010)

The entry of private insurance companies transformed the Indian insurance landscape. Between 2000 and 2010, numerous private players entered both the life and general insurance sectors. These companies brought with them new products, new distribution channels, and new ways of thinking about insurance.

In life insurance, private companies like HDFC Life, ICICI Prudential, SBI Life, Max Life, and Bajaj Allianz emerged as significant players. These companies introduced innovative products such as unit-linked insurance plans (ULIPs), which combined insurance protection with investment returns. They also developed specialized products for different customer segments, from high-net-worth individuals to rural customers.

The general insurance sector saw similar transformation with the entry of companies like ICICI Lombard, Bajaj Allianz General Insurance, HDFC ERGO, and Reliance General Insurance. These companies brought new approaches to motor insurance, health insurance, and commercial insurance. They introduced cashless hospitalization, direct claim settlement, and other customer-friendly features.

Competition led to significant improvements in customer service. Insurers invested in technology to speed up policy issuance and claims settlement. They developed multiple distribution channels, including bank branches, brokers, and eventually digital platforms. They trained their agents better and implemented quality control measures.

The period also saw the development of specialized insurance companies. Standalone health insurance companies like Star Health and Allied Insurance focused exclusively on health coverage, bringing expertise and innovation to this important segment. Reinsurance companies expanded their operations in India, providing capacity and risk management support to primary insurers.

However, the rapid growth also brought challenges. The aggressive selling of ULIPs led to concerns about mis-selling and inappropriate products being sold to unsuspecting customers. IRDAI had to step in with regulations to protect policyholders and ensure that insurance products were sold appropriately. The regulatory framework evolved continuously to address emerging issues and ensure the healthy development of the sector.

Digital Transformation: The InsurTech Revolution (2010-Present)

The last decade has witnessed a technological revolution in the Indian insurance sector. The proliferation of smartphones, the expansion of internet connectivity, and the government’s push for digitalization have transformed how insurance is bought, sold, and serviced.

Digital insurance platforms have made it possible for customers to compare policies, calculate premiums, and purchase insurance online within minutes. Companies like Policybazaar, Coverfox, and InsuranceDekho have emerged as major insurance aggregators, providing customers with choice and transparency. These platforms have democratized access to insurance information and empowered customers to make informed decisions.

InsurTech startups have brought innovation to every aspect of the insurance value chain. Companies like Acko General Insurance and Go Digit have built fully digital insurance models, eliminating paperwork and reducing costs. They use artificial intelligence and machine learning for underwriting, claims processing, and fraud detection. Their digital-first approach has appealed particularly to young, tech-savvy customers.

The COVID-19 pandemic accelerated digital adoption in insurance. With physical interactions limited, insurers had to rapidly digitize their operations. Video-based medical examinations for life insurance, digital Know Your Customer (KYC) processes, and online claims submission became the norm. Many first-time insurance buyers turned to digital channels, and the habit of buying insurance online is likely to persist.

IRDAI has supported digital transformation through various initiatives. The regulatory sandbox has allowed insurers to test innovative digital products. The Bima Sugam portal, being developed as a one-stop platform for insurance, aims to bring together all stakeholders on a common digital infrastructure. The Ayushman Bharat Digital Mission is creating a framework for digital health records that could transform health insurance.

Artificial intelligence and big data analytics are being used to personalize insurance products and pricing. Telematics devices in vehicles enable usage-based motor insurance, where premiums are based on actual driving behavior. Wearable devices allow health insurers to reward healthy lifestyles with lower premiums. These innovations are making insurance more relevant and fair for customers.

Government Schemes: Insurance for the Masses

The Indian government has launched several ambitious insurance schemes aimed at providing financial protection to vulnerable sections of society. These schemes represent a recognition that market-based insurance alone cannot achieve universal coverage, and government intervention is necessary to reach the poorest and most marginalized.

The Pradhan Mantri Jan Dhan Yojana, launched in 2014, included insurance components along with bank accounts. The Pradhan Mantri Jeevan Jyoti Bima Yojana provides life insurance coverage of Rs. 2 lakh at a highly subsidized premium. The Pradhan Mantri Suraksha Bima Yojana offers accidental death and disability coverage at an affordable price. These schemes have brought millions of low-income families into the insurance fold for the first time.

Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY), launched in 2018, is the world’s largest public health insurance scheme. It provides health coverage of up to Rs. 5 lakh per family per year for secondary and tertiary care hospitalization to over 10 crore vulnerable families. The scheme has been a game-changer for healthcare access, enabling poor families to avail quality medical treatment without worrying about costs.

In September 2024, the government expanded AB-PMJAY to cover all senior citizens above 70 years of age, irrespective of their socio-economic status. This expansion will provide crucial health protection to millions of elderly Indians who are often most vulnerable to health-related financial shocks.

The government has also promoted crop insurance through schemes like the Pradhan Mantri Fasal Bima Yojana, which protects farmers against crop losses due to natural calamities. These agricultural insurance schemes are crucial for managing risk in a sector where millions depend on rainfall and weather conditions for their livelihood.

Current State of the Indian Insurance Sector (2024-2025)

The Indian insurance sector today is a dynamic and growing industry that plays a vital role in the country’s financial system. According to IRDAI’s annual report for 2024-25, the sector issued 41.84 crore policies, collected premiums of Rs. 11.93 lakh crore, paid claims of Rs. 8.36 lakh crore, and reported assets under management of Rs. 74.44 lakh crore.

India is now the 10th largest insurance market globally by nominal premium volumes, with a market share of 1.8 percent. However, insurance penetration in India remains low at 3.7 percent of GDP, compared to the global average of 7.3 percent. Life insurance penetration is 2.7 percent, while non-life insurance penetration is just 1 percent. This gap represents both a challenge and an enormous opportunity for growth.

Insurance density, which measures per capita premium spending, stands at USD 97 in India, compared to the global average of USD 943. This indicates significant headroom for growth as incomes rise and insurance awareness increases. The life insurance industry recorded premium income of Rs. 8.86 lakh crore in 2024-25, registering a growth of 6.73 percent.

The sector is characterized by a mix of public and private players. In life insurance, LIC continues to dominate with a market share of around 58-60 percent by premium and over 70 percent by policy count. However, private sector insurers are growing faster, with a growth rate of 12.07 percent compared to LIC’s 2.75 percent. In general insurance, private companies have a larger market share than public sector insurers.

The InsurTech sector in India has emerged as a significant growth driver. With over 150 active players, cumulative valuations exceeding USD 15.8 billion, and revenues of USD 0.9 billion in 2024, the InsurTech ecosystem has grown tenfold since 2019. The sector has produced two unicorns and numerous successful startups that are transforming insurance through technology.

Challenges and Opportunities Ahead

Despite significant progress, the Indian insurance sector faces numerous challenges. Low penetration and density remain the most pressing issues. Millions of Indians remain uninsured or underinsured, leaving them vulnerable to financial shocks from death, illness, accidents, or property loss.

The sector also faces challenges in distribution. While urban India has good access to insurance products and services, rural areas remain underserved. The cost of serving remote customers, the lack of awareness about insurance, and the challenge of collecting premiums from low-income customers all contribute to this gap.

Claims settlement remains an area of concern. While insurers have improved their claims processes, delays and disputes still occur. Building trust with customers requires consistent, fair, and speedy claims settlement. The industry needs to continue investing in technology and processes to improve the claims experience.

Regulatory compliance is becoming increasingly complex as the sector grows and evolves. Insurers must navigate a web of regulations while remaining agile and competitive. Balancing innovation with consumer protection is a constant challenge for both insurers and regulators.

However, the opportunities far outweigh the challenges. India’s demographic profile is favorable for insurance growth. A young population entering the workforce, rising incomes, increasing urbanization, and growing awareness about financial planning all bode well for the sector. The protection gap in India is estimated to be enormous, representing a massive untapped market.

Technology will continue to be a key enabler of growth. Artificial intelligence and generative AI present a USD 4 billion profit expansion opportunity for the Indian insurance industry. Digital distribution can dramatically reduce costs and expand reach. Data analytics can improve underwriting and enable personalized products.

The government’s vision of “Insurance for All by 2047” provides a clear roadmap for the sector. This ambitious goal aims to ensure that every Indian has access to appropriate insurance coverage by the time India completes 100 years of independence. Achieving this vision will require coordinated efforts from insurers, regulators, government, and other stakeholders.

The Future of Insurance in India

Looking ahead, the Indian insurance sector is poised for transformative growth. Several trends are likely to shape the industry in the coming years.

Embedded insurance, where coverage is integrated into the purchase of products and services, is expected to grow rapidly. When you buy a smartphone, travel ticket, or consumer durable, insurance will be offered seamlessly as part of the transaction. This will bring insurance to customers who might not actively seek it out.

Parametric insurance, which pays out based on predefined triggers rather than actual loss assessment, could revolutionize areas like crop insurance and disaster coverage. Satellite data, weather stations, and IoT devices can trigger automatic payouts when specific conditions are met, making claims settlement faster and more transparent.

Usage-based insurance models will become more prevalent. Instead of paying fixed premiums based on broad risk categories, customers will pay based on their actual usage and behavior. Safe drivers will pay less for motor insurance, healthy individuals will get discounts on health insurance, and businesses will pay premiums that reflect their actual risk exposure.

Microinsurance will expand to reach low-income customers with products designed for their specific needs and ability to pay. Flexible premium payment options, simplified products, and innovative distribution through community-based organizations and mobile networks will make insurance accessible to millions who are currently excluded.

The convergence of insurance with healthcare, wellness, and financial services will create new value propositions. Health insurers will become health partners, offering preventive care and wellness programs along with coverage. Life insurers will offer comprehensive financial planning solutions that go beyond traditional insurance products.

The evolution of insurance in India is a remarkable story of transformation. From its ancient philosophical roots to the colonial-era beginnings, from the nationalization era to the liberalization boom, from traditional paper-based processes to digital-first models, the journey has been long and eventful.

Today, the Indian insurance sector stands at an inflection point. With over 1.4 billion people, a growing economy, rising awareness about financial protection, and supportive government policies, the conditions are ripe for explosive growth. The sector has the potential to become one of the largest in the world while serving the critical social function of providing financial security to millions.

The challenges are significant but not insurmountable. Low penetration, distribution challenges, and trust deficits can be addressed through technology, innovation, and customer-centric approaches. The regulatory environment is supportive of growth while ensuring policyholder protection. The government’s commitment to universal insurance coverage provides a strong policy tailwind.

As India moves toward its goal of becoming a developed economy by 2047, insurance will play a crucial role in this transformation. It will provide the financial protection that enables individuals and families to take risks, invest in their futures, and weather life’s uncertainties. It will mobilize long-term savings for infrastructure development and economic growth. It will contribute to social stability by preventing families from falling into poverty due to unexpected losses.

The story of insurance in India is far from complete. The next chapter, being written today through digital innovation, regulatory evolution, and market expansion, promises to be the most exciting yet. For the millions of Indians who will gain financial protection for the first time, and for the economy that will benefit from a stronger, more resilient financial system, the evolution of insurance in India is a journey worth watching and supporting.