Insurance serves as a vital financial safety net that protects individuals and families from unexpected hardships. Whether it is life insurance that secures your family’s future, health insurance that covers medical expenses, or motor insurance that protects your vehicle, these policies provide peace of mind during challenging times. But have you ever wondered who ensures that insurance companies operate fairly and honor their commitments to policyholders? This crucial responsibility lies with the Insurance Regulatory and Development Authority of India, commonly known as IRDAI.

The Insurance Regulatory and Development Authority of India (IRDAI) serves as the guardian of the insurance sector in India. Established as an autonomous statutory body,IRDAI operates under the Ministry of Finance and oversees the entire insurance ecosystem, including life insurance, general insurance, and health insurance companies. Its primary mission is to protect policyholders’ interests while promoting the healthy growth and development of the insurance industry. Through comprehensive regulations, monitoring mechanisms, and consumer protection initiatives, IRDAI ensures that insurance remains a trustworthy and reliable financial tool for millions of Indians.

This article explores the multifaceted role of IRDAI in safeguarding policyholder interests, examining its functions, regulatory framework, grievance redressal mechanisms, and recent reforms that have strengthened consumer protection in the Indian insurance sector. Understanding these aspects empowers policyholders to make informed decisions and seek appropriate remedies when needed.

The importance of IRDAI in the lives of ordinary Indians cannot be overstated. When a family loses its breadwinner and looks to a life insurance policy for financial support, when a patient needs urgent medical treatment covered by health insurance, or when a farmer seeks compensation for crop damage, the effectiveness of insurance regulation directly impacts their lives. IRDAI’s vigilant oversight ensures that these moments of crisis do not become moments of betrayal, where promises made in policy documents are broken by insurers.

Figure 1: IRDAI’s Regulatory Oversight Protecting Indian Policyholders

The Birth and Evolution of IRDAI

The story of IRDAI begins with the transformation of India’s insurance sector from a government-controlled monopoly to a regulated competitive market. Before the establishment of IRDAI, the insurance industry in India was entirely under government control. Life insurance was nationalized in 1956, leading to the creation of the Life Insurance Corporation of India (LIC), while general insurance followed suit in 1972 with the formation of the General Insurance Corporation (GIC). This nationalized structure remained unchanged for several decades.

The winds of change began with the economic liberalization of the 1990s. Recognizing the need for reform in the insurance sector, the Government of India appointed the Malhotra Committee in 1993 to examine the industry and recommend changes. The committee’s report laid the foundation for opening up the insurance sector to private players while establishing an independent regulatory body to oversee operations.

The Insurance Regulatory and Development Authority Act was passed by Parliament in 1999, formally establishing IRDAI as a statutory body. The authority became operational in 2000, marking a new era for the Indian insurance industry. This transformation allowed private insurance companies, including those with foreign partnerships, to enter the market, bringing innovation, competition, and improved services to Indian consumers.

Since its inception, IRDAI has evolved significantly, adapting to changing market dynamics, technological advancements, and consumer needs. The regulator has continuously refined its framework to balance industry growth with robust policyholder protection, making the Indian insurance sector one of the most regulated and consumer-friendly markets globally.

The transition from a nationalized monopoly to a competitive market with more than 50 insurance companies operating today has been remarkable. This transformation would not have been possible without a strong regulatory framework that ensures fair competition while protecting consumer interests. IRDAI has successfully navigated this complex transition, learning from international best practices while adapting regulations to suit Indian conditions and requirements.

The structure of IRDAI consists of a ten-member body appointed by the Government of India, including a Chairman, five whole-time members, and four part-time members. This diverse composition brings together expertise from various fields including finance, law, actuarial science, and administration, ensuring well-rounded regulatory oversight. The authority operates through various departments specializing in life insurance, general insurance, health insurance, actuarial matters, legal affairs, and consumer protection.

Key Objectives of IRDAI

The mission of IRDAI, as defined in the IRDA Act of 1999, encompasses multiple objectives that collectively serve the interests of policyholders and the insurance industry. Understanding these objectives provides insight into how IRDAI approaches its regulatory responsibilities.

Protection of Policyholders’ Interests

The foremost objective of IRDAI is to protect the interests of policyholders. This involves ensuring that insurance companies treat customers fairly, honor their contractual obligations, and maintain transparency in all dealings. IRDAI achieves this through comprehensive regulations governing policy terms, claim settlements, premium calculations, and disclosure requirements.

Regulation and Promotion of Orderly Growth

IRDAI is tasked with regulating the insurance industry to ensure orderly growth. This includes granting licenses to new insurers, monitoring existing companies’ operations, and enforcing compliance with regulatory standards. The authority balances strict regulation with measures that encourage innovation and expansion, creating an environment where the insurance sector can thrive while maintaining high standards of service.

Ensuring Financial Soundness

A critical objective is ensuring that insurance companies remain financially sound and capable of meeting their obligations to policyholders. IRDAI enforces solvency requirements, monitors financial performance, and takes corrective action when companies face financial difficulties. This protects policyholders from the risk of their insurer becoming insolvent and unable to pay claims.

Promoting Fair Competition

IRDAI fosters a competitive insurance market that benefits consumers through better products, improved services, and competitive pricing. By preventing monopolistic practices and ensuring a level playing field, the regulator encourages insurers to innovate and improve their offerings continuously.

Increasing Insurance Penetration and Awareness

A significant objective of IRDAI is to increase insurance awareness and penetration across India, particularly in rural and underserved areas. The authority mandates insurers to allocate a portion of their business to rural and social sectors, ensuring that insurance reaches those who need it most. Through various awareness campaigns and educational initiatives, IRDAI helps citizens understand the importance of insurance and make informed decisions about their financial security.

Ensuring Speedy Settlement of Genuine Claims

Nothing damages trust in insurance more than delayed or denied legitimate claims. IRDAI places strong emphasis on ensuring that insurers settle genuine claims promptly and fairly. The authority monitors claim settlement ratios, turnaround times, and reasons for claim repudiation, taking action against insurers that consistently fail to meet standards. This focus on claim settlement ensures that policyholders receive the protection they paid for when they need it most.

Core Functions of IRDAI in Policyholder Protection

IRDAI performs numerous functions that directly or indirectly protect policyholder interests. These functions span the entire insurance lifecycle, from company registration to claim settlement and grievance resolution.

Regulatory Framework and Licensing

Before any insurance company can operate in India, it must obtain a license from IRDAI. The licensing process is rigorous, evaluating applicants based on capital adequacy, management expertise, business plans, and commitment to policyholder protection. This ensures that only credible and financially stable entities enter the market. IRDAI also regulates insurance intermediaries, including agents, brokers, and third-party administrators, establishing qualification requirements and codes of conduct to ensure ethical practices.

Solvency Regulation and Financial Stability

One of IRDAI’s most crucial functions is monitoring the financial health of insurance companies. The authority mandates that insurers maintain a minimum solvency margin, which represents the excess of assets over liabilities. This requirement ensures that companies have adequate financial reserves to meet their obligations to policyholders, even during adverse circumstances. IRDAI conducts regular inspections and audits to assess insurers’ financial soundness and takes prompt action if solvency concerns arise.

Product Approval and Premium Regulation

IRDAI reviews and approves insurance products before they can be offered to consumers. This approval process ensures that policy terms are fair, transparent, and provide adequate coverage. The authority also regulates premium rates for certain insurance products, particularly third-party motor insurance, to prevent overcharging and ensure affordability. For products where insurers have pricing flexibility, IRDAI monitors rates to detect and prevent exploitative practices.

Claim Settlement Monitoring

The true test of an insurance policy comes at the time of claim settlement. IRDAI closely monitors insurers’ claim settlement ratios and turnaround times, ensuring that genuine claims are paid promptly and fairly. The authority has established strict timelines for claim processing and requires insurers to provide detailed explanations when claims are rejected. Policyholders can approach IRDAI if they face unreasonable delays or unfair claim denials.

Market Conduct Regulation

IRDAI actively monitors the market conduct of insurance companies to prevent mis-selling, unfair practices, and deceptive marketing. The authority has issued detailed guidelines on advertisements, prohibiting misleading claims and requiring clear disclosure of policy terms. Insurers must obtain approval for certain types of advertisements, and violations can result in penalties. This oversight ensures that policyholders are not lured into purchasing unsuitable products through false promises or incomplete information.

Investment Regulation

Insurance companies collect premiums from policyholders with the promise of paying future claims. These funds must be invested prudently to ensure both safety and reasonable returns. IRDAI specifies detailed investment guidelines that dictate how insurers can deploy their funds, specifying limits for different asset classes and requiring diversification to minimize risk. These regulations protect policyholders’ money and ensure that insurers can meet their long-term obligations.

Rural and Social Sector Obligations

IRDAI mandates that insurance companies allocate a specified percentage of their business to rural areas and socially vulnerable sections. This ensures that insurance penetration extends beyond urban centers and affluent populations to reach farmers, workers, and marginalized communities. Life insurers must meet specified targets for rural policies and lives covered, while general insurers must provide coverage for crops, livestock, and rural assets. These obligations help democratize access to financial protection across India’s diverse population.

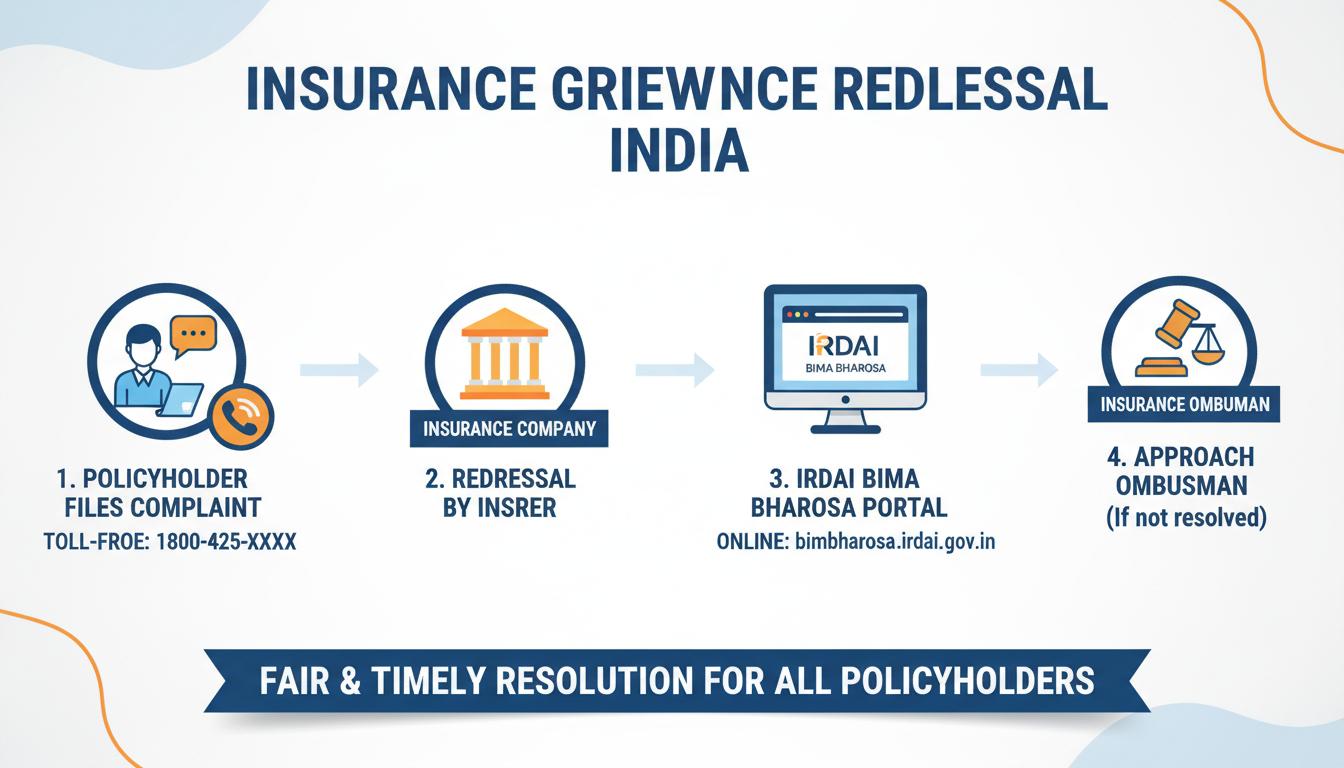

Grievance Redressal Mechanisms

Despite the best regulatory framework, disputes between policyholders and insurers can arise. IRDAI has established multiple channels for grievance redressal, ensuring that policyholders have access to fair and efficient resolution mechanisms.

Bima Bharosa: The Integrated Grievance Management System

Bima Bharosa, formerly known as the Integrated Grievance Management System (IGMS), is IRDAI’s flagship platform for addressing policyholder complaints. This comprehensive online system allows policyholders to register complaints, track their status, and receive updates in real-time. The portal serves as a centralized repository of industry-wide grievance data, enabling IRDAI to monitor complaint patterns and take corrective action against insurers with poor grievance handling records.

Policyholders can access Bima Bharosa through multiple channels. The online portal at bimabharosa.irdai.gov.in provides a user-friendly interface for complaint registration. Alternatively, complaints can be filed via email at complaints@irdai.gov.in or through the toll-free numbers 155255 and 1800-425-4732. The IRDAI Grievance Call Centre, also known as Bima Shikayat, provides assistance in multiple languages and guides policyholders through the complaint process.

Once a complaint is registered in Bima Bharosa, it is forwarded to the respective insurance company for resolution. The system tracks turnaround times and sends alerts when deadlines approach. If the insurer fails to resolve the complaint within the stipulated timeframe, or if the policyholder is dissatisfied with the resolution, the matter can be escalated for further action.

The effectiveness of Bima Bharosa lies in its transparency and accountability. Policyholders receive a unique token number for tracking their complaint status. The system captures the entire lifecycle of a complaint from registration to resolution, creating an audit trail that helps identify systemic issues and persistent offenders. Insurers with poor grievance handling records face regulatory scrutiny and potential penalties, creating strong incentives for timely and fair resolution.

IRDAI has established clear timelines for complaint resolution. Insurance companies are expected to acknowledge complaints within a few days and resolve them within specified periods depending on the complexity. If the insurer fails to respond satisfactorily, policyholders can escalate the matter to IRDAI for intervention. The authority can then take up the complaint with the insurer, conduct investigations, and direct appropriate action.

Figure 2: The Insurance Grievance Redressal Process in India

Insurance Ombudsman: An Alternative Dispute Resolution

The Insurance Ombudsman scheme provides an independent, cost-effective, and efficient mechanism for resolving insurance disputes outside the court system. Established under the Insurance Ombudsman Rules, 2017, this quasi-judicial body offers policyholders a accessible avenue for seeking redressal without the expenses and delays associated with litigation.

Currently, there are 17 Insurance Ombudsman centers located across major cities in India, including Delhi, Mumbai, Kolkata, Chennai, Bangalore, Hyderabad, and others. Policyholders can approach the Ombudsman office within whose jurisdiction their insurance company’s branch is located or where they reside. The Ombudsman can consider complaints with a claim value of up to Rs. 50 lakh, as amended in 2023.

The Ombudsman can address various types of complaints, including delays in claim settlement, partial or total repudiation of claims, disputes regarding premium payments, misrepresentation of policy terms, and policy servicing issues. The process begins with the Ombudsman attempting mediation and conciliation between the parties. If a settlement is reached and accepted by the policyholder, the insurer must comply within 15 days.

If mediation fails, the Ombudsman can pass an award based on the merits of the case. This award is binding on the insurance company, which must comply within 30 days. However, the policyholder retains the right to accept or reject the award. If dissatisfied, policyholders can still pursue legal remedies through consumer courts or civil courts. The entire process is free of cost for policyholders, making it an accessible option for all.

The Insurance Ombudsman mechanism has proven highly effective in resolving disputes without the need for expensive and time-consuming litigation. The informal procedures, simplified documentation requirements, and focus on fair settlement make it an attractive option for policyholders seeking redressal. The Ombudsman’s offices are staffed by experienced professionals with expertise in insurance matters, ensuring that complaints are evaluated by knowledgeable individuals who understand the nuances of insurance contracts and industry practices.

Policyholders should note that approaching the Ombudsman requires following a specific procedure. First, they must have filed a complaint with the insurance company and allowed reasonable time for resolution. The complaint to the Ombudsman must be filed within one year of the insurer’s final response or the date by which a response should have been received. The complaint must be in writing, either physically or electronically, and should include relevant documents such as the policy copy, correspondence with the insurer, and the repudiation letter if applicable.

Recent Reforms and Policyholder Protection Regulations

IRDAI has been proactive in updating its regulatory framework to enhance policyholder protection and adapt to changing market realities. The year 2024 witnessed significant reforms that have strengthened consumer rights and streamlined insurance operations.

The IRDAI (Protection of Policyholders’ Interests, Operations, and Allied Matters of Insurers) Regulations, 2024

These comprehensive regulations represent a major overhaul of policyholder protection norms. Key provisions include an extended free look period of 30 days from the receipt of the policy document, giving policyholders adequate time to review their purchase decision. The regulations also mandate electronic issuance of policies with the option for physical copies upon request, promoting efficiency while accommodating diverse preferences.

The 2024 regulations strengthen grievance redressal requirements, mandating insurers to establish comprehensive systems with clear timelines for resolution. They also introduce enhanced disclosure requirements, ensuring that policyholders receive complete information about policy terms, benefits, exclusions, and charges in a clear and understandable format.

Customer Information Sheet (CIS)

A significant innovation introduced by IRDAI is the mandatory Customer Information Sheet (CIS). This standardized document provides policyholders with a concise summary of key policy details, including coverage, exclusions, premium payment terms, and claim procedures. The CIS must be provided in simple language, making it easier for policyholders to understand their insurance coverage without wading through lengthy policy documents.

Health Insurance Portability

IRDAI has facilitated health insurance portability, allowing policyholders to transfer their existing policies to another insurer without losing benefits accumulated under the current policy. This includes credit for waiting periods served and no-claim bonuses earned. Portability promotes competition among insurers and gives policyholders the freedom to choose better service without penalty.

Enhanced Penalties and Enforcement

Recent amendments to insurance laws have significantly increased the penalties that IRDAI can impose for regulatory violations. The maximum penalty has been raised from Rs. 1 crore to Rs. 10 crore, providing a stronger deterrent against unfair practices. Additionally, IRDAI now has disgorgement powers, enabling it to order entities to surrender wrongful gains made through regulatory violations. Personal liability provisions have also been introduced for directors and officers who knowingly participate in violations.

Data Protection and Privacy

Recognizing the sensitive nature of policyholder information, recent regulatory updates have strengthened data protection requirements. The amendments introduce a statutory basis for protecting and sharing policyholder information, limiting disclosure to circumstances where express consent is obtained, where required by law, or where there is a public duty to disclose. These provisions align with the Digital Personal Data Protection Act, 2023, ensuring that policyholders’ personal and financial information remains secure.

Streamlined Operations and Self-Regulation

The 2024 regulations mark a shift toward principle-based regulation and self-governance by insurers. While maintaining strong oversight, IRDAI has removed certain prescriptive requirements, allowing insurers greater flexibility in designing their processes while holding them accountable for outcomes. For example, insurers no longer need prior approval for opening offices that meet specified criteria, and advertisement filing requirements have been replaced with board-approved policies overseen by designated personnel. This approach reduces administrative burden while maintaining robust consumer protection standards.

Consumer Education and Awareness Initiatives

IRDAI recognizes that informed consumers are better equipped to protect their interests. The authority conducts extensive awareness campaigns through various media channels, including television, radio, print, and digital platforms. These campaigns educate the public about the importance of insurance, how to choose appropriate products, and how to file complaints when needed.

The Policyholders’ Protection and Grievance Redressal Department actively disseminates information about policyholder rights and available redressal mechanisms. Advertisements are released in English, Hindi, and regional languages to ensure widespread reach. IRDAI also collaborates with consumer organizations, industry bodies, and educational institutions to promote insurance literacy.

The authority’s website, irdai.gov.in, serves as a comprehensive resource for policyholders, providing information about registered insurers, approved products, grievance procedures, and regulatory updates. The Bima Bharosa portal not only handles complaints but also educates users about their rights and the complaint resolution process.

IRDAI has also implemented the Insurance Information Bureau (IIB), which collects and disseminates industry-wide data to help consumers make informed choices. The IIB provides information about claim settlement ratios of different insurers, enabling policyholders to compare companies based on their track record of honoring claims. This transparency promotes competition based on service quality and encourages insurers to improve their claims handling processes.

Special initiatives target vulnerable populations who may be less familiar with insurance concepts. Rural awareness camps, multilingual educational materials, and collaborations with self-help groups and microfinance institutions help extend insurance literacy to underserved communities. These efforts are crucial for achieving IRDAI’s vision of universal insurance coverage, as informed consumers are more likely to purchase appropriate products and utilize them effectively when needed.

The Road Ahead: Insurance for All by 2047

IRDAI has articulated an ambitious vision of “Insurance for All by 2047,” aligning with India’s centenary of independence. This vision aims to ensure that every Indian citizen has access to appropriate insurance coverage, providing financial security and resilience against life’s uncertainties.

To achieve this goal, IRDAI is implementing measures to increase insurance penetration across underserved segments, including rural populations, low-income households, and vulnerable sections of society. The authority is promoting innovative products, leveraging technology for wider distribution, and simplifying processes to make insurance more accessible and affordable.

The regulatory framework continues to evolve toward a principle-based approach, giving insurers greater flexibility while maintaining strong consumer protection standards. IRDAI is also embracing digital transformation, promoting online policy issuance, digital claims processing, and AI-powered grievance handling to improve efficiency and customer experience.

As the insurance sector grows and evolves, IRDAI remains committed to its core mission of protecting policyholder interests. The authority continues to balance innovation with regulation, ensuring that the benefits of a dynamic insurance market reach all segments of society while safeguarding consumers from potential risks and unfair practices.

Technology will play a crucial role in achieving these goals. IRDAI is promoting the use of artificial intelligence and machine learning for fraud detection, claims processing, and customer service. The regulator is also encouraging the development of insurtech solutions that make insurance more accessible, affordable, and user-friendly. At the same time, IRDAI is establishing frameworks for regulating emerging technologies and business models to ensure that innovation does not come at the cost of consumer protection.

The regulatory sandbox approach allows insurers to test innovative products and services in a controlled environment before full-scale launch. This promotes innovation while ensuring that new offerings meet regulatory standards and genuinely benefit consumers. IRDAI’s proactive stance on innovation positions India as a leader in insurance regulation globally, with other countries looking to the Indian model for inspiration.

The Insurance Regulatory and Development Authority of India plays a pivotal role in safeguarding the interests of millions of policyholders across the country. Through its comprehensive regulatory framework, robust monitoring mechanisms, and accessible grievance redressal systems, IRDAI ensures that insurance remains a reliable financial safety net for Indian families.

From licensing insurers and approving products to monitoring claim settlements and resolving disputes, IRDAI’s functions touch every aspect of the insurance ecosystem. Recent reforms have further strengthened consumer protection, introducing measures like extended free look periods, mandatory Customer Information Sheets, and enhanced penalties for violations.

For policyholders, understanding IRDAI’s role empowers them to make informed decisions and seek appropriate remedies when needed. The Bima Bharosa portal and Insurance Ombudsman scheme provide accessible channels for addressing grievances, while the authority’s awareness initiatives help consumers navigate the complex world of insurance with confidence.

As India moves toward the goal of Insurance for All by 2047, IRDAI’s role becomes even more critical. The authority’s continued commitment to balancing industry growth with robust consumer protection will ensure that insurance fulfills its promise of financial security for every Indian citizen. In this journey, policyholders can take comfort in knowing that a dedicated regulatory body stands guard over their interests, working tirelessly to make the insurance sector fairer, more transparent, and more responsive to their needs.

The success of IRDAI’s mission depends not only on regulatory frameworks but also on the active engagement of policyholders. By understanding their rights, asking the right questions before purchasing policies, maintaining proper documentation, and utilizing available grievance channels when needed, policyholders can protect themselves and contribute to a healthier insurance ecosystem. Informed and assertive consumers drive insurers to improve their services and comply with regulatory standards, creating a virtuous cycle of improvement.

Looking ahead, the Indian insurance sector is poised for significant transformation. Demographic changes, rising incomes, increasing awareness, and technological advancement will drive growth in insurance penetration. Climate change, evolving health risks, and changing lifestyles will create new challenges that require innovative insurance solutions. IRDAI’s adaptive regulatory approach will be essential in navigating these changes while maintaining the fundamental promise of insurance: protection when it matters most.

In conclusion, the Insurance Regulatory and Development Authority of India stands as a pillar of trust in the financial lives of millions of Indians. Its comprehensive approach to regulation, combining strict oversight with encouragement of innovation, has created an insurance sector that is both dynamic and dependable. As policyholders navigate the complex world of insurance, they can do so with confidence, knowing that IRDAI works continuously to protect their interests and ensure that the insurance industry serves its true purpose: providing financial security and peace of mind to all.