Taxes are an essential part of life in the United States, yet many Americans find the tax system confusing and overwhelming. Whether you are a first-time filer or someone who has been paying taxes for decades, understanding how the system works can help you make better financial decisions, avoid costly mistakes, and potentially save money. This comprehensive guide breaks down the American tax system into simple, easy-to-understand concepts that anyone can grasp.

At its core, taxation is the way governments collect money from individuals and businesses to fund public services and government operations. In the United States, taxes are collected at three levels: federal, state, and local. Each level has its own set of rules, rates, and purposes. The federal government collects the majority of taxes, which fund national programs like defense, Social Security, Medicare, and interest on the national debt. State governments collect taxes to fund education, transportation, and state-specific programs. Local governments rely on taxes to provide essential services like police and fire protection, public schools, and road maintenance.

The United States operates under a progressive tax system, which means that people with higher incomes pay a higher percentage of their income in taxes than those with lower incomes. This principle is based on the idea that those who have more financial resources can afford to contribute more to support public services. However, the reality of the tax system is more complex, with numerous deductions, credits, and exemptions that can significantly affect how much you actually pay.

Understanding taxes is not just about knowing how much you owe. It is about understanding your rights and responsibilities as a taxpayer, knowing what deductions and credits you qualify for, and being able to plan your finances effectively. With the right knowledge, you can minimize your tax burden legally and ensure that you are not paying more than necessary.

Types of Taxes in the United States

The American tax system includes several different types of taxes, each with its own rules and purposes. Understanding these different taxes is crucial for getting a complete picture of how taxation works in the United States.

Federal Income Tax

Federal income tax is the largest source of revenue for the United States government. It is a tax on the income earned by individuals, corporations, trusts, and other legal entities. The federal income tax system is progressive, meaning that tax rates increase as income increases. The Internal Revenue Service (IRS) is the federal agency responsible for collecting income taxes and enforcing tax laws.

For individuals, federal income tax applies to various types of income, including wages and salaries, self-employment income, investment income, rental income, and certain other types of earnings. Employers typically withhold federal income tax from employees’ paychecks throughout the year based on the information provided on Form W-4. Self-employed individuals and those with significant non-wage income are generally required to make quarterly estimated tax payments.

The amount of federal income tax you owe depends on your taxable income, which is your total income minus certain deductions and exemptions. The tax code provides numerous deductions, such as those for mortgage interest, charitable contributions, and state and local taxes, which can reduce your taxable income. Additionally, tax credits, such as the Child Tax Credit and the Earned Income Tax Credit, can directly reduce the amount of tax you owe.

State and Local Taxes

In addition to federal taxes, most Americans also pay state and local taxes. There are significant variations in tax policies across different states. Some states, like Florida and Texas, have no state income tax at all, while others, like California and New York, have relatively high state income tax rates. State income taxes are generally calculated similarly to federal income taxes, though the specific rates and brackets vary by state.

Local taxes can include city or county income taxes, property taxes, and various fees. These taxes fund local services such as public schools, police and fire departments, road maintenance, and parks and recreation facilities. Property taxes are typically the largest source of revenue for local governments and are based on the assessed value of real estate.

Payroll Taxes

Payroll taxes are taxes withheld from employees’ wages and paid by employers to fund specific social insurance programs. The two main payroll taxes are Social Security tax and Medicare tax, collectively known as FICA taxes (Federal Insurance Contributions Act). Employees pay 6.2% of their wages for Social Security and 1.45% for Medicare, with employers matching these amounts. Self-employed individuals pay both the employee and employer portions, totaling 15.3%.

Social Security taxes fund the Social Security program, which provides retirement, disability, and survivor benefits to eligible workers and their families. Medicare taxes fund the Medicare program, which provides health insurance for people aged 65 and older, as well as certain younger individuals with disabilities. There is a wage cap on Social Security taxes, meaning that earnings above a certain threshold are not subject to Social Security tax. For 2026, this cap is expected to be around $176,000.

Sales and Property Taxes

Sales taxes are consumption taxes imposed on the sale of goods and services. The United States does not have a federal sales tax, but most states and many local jurisdictions impose sales taxes. Sales tax rates vary widely, from 0% in states like Delaware, Montana, New Hampshire, and Oregon, to over 9% in some localities when state and local rates are combined. Some states exempt certain items, such as groceries and prescription medications, from sales tax.

Property taxes are taxes on real estate and, in some jurisdictions, personal property such as vehicles and business equipment. These taxes are typically based on the assessed value of the property and are collected by local governments. Property tax rates vary significantly depending on the location and the specific needs of the local government. Homeowners can often deduct property taxes on their federal income tax returns, though there are limits to this deduction.

Figure 1: Understanding tax forms and calculations is essential for every American taxpayer.

How Income Tax Works

Understanding how federal income tax works is essential for every American taxpayer. The process involves several key steps: calculating your gross income, determining your adjusted gross income, subtracting deductions to arrive at taxable income, applying the appropriate tax rates, and then subtracting any tax credits to determine your final tax liability.

Tax Brackets and Rates

The United States uses a marginal tax rate system with seven tax brackets. This means that different portions of your income are taxed at different rates. For the 2026 tax year, the federal income tax brackets for single filers are expected to be approximately: 10% on income up to $11,925, 12% on income from $11,926 to $48,475, 22% on income from $48,476 to $103,350, 24% on income from $103,351 to $197,300, 32% on income from $197,301 to $250,525, 35% on income from $250,526 to $626,350, and 37% on income above $626,350.

It is important to understand that moving into a higher tax bracket does not mean all of your income is taxed at the higher rate. Only the income that falls within that bracket is taxed at the higher rate. For example, if you are a single filer with $60,000 of taxable income, you do not pay 22% on the entire amount. Instead, you pay 10% on the first $11,925, 12% on the next $36,550, and 22% only on the remaining $11,525.

Tax brackets are adjusted annually for inflation, which means the income thresholds for each bracket increase slightly each year. This prevents what is known as “bracket creep,” where inflation pushes taxpayers into higher tax brackets even though their real purchasing power has not increased.

Deductions and Credits

Deductions and credits are two of the most important tools for reducing your tax liability, but they work in different ways. Deductions reduce the amount of income that is subject to tax, while credits directly reduce the amount of tax you owe. A $1,000 deduction might save you $220 in taxes if you are in the 22% tax bracket, but a $1,000 credit saves you a full $1,000 in taxes.

Taxpayers can choose between taking the standard deduction or itemizing their deductions. The standard deduction is a fixed amount that varies based on your filing status. For 2026, the standard deduction is expected to be approximately $15,000 for single filers and $30,000 for married couples filing jointly. Itemized deductions include things like mortgage interest, state and local taxes (up to $10,000), charitable contributions, and medical expenses exceeding a certain percentage of your income. You should choose whichever method gives you the larger deduction.

Above-the-line deductions, also known as adjustments to income, can be taken regardless of whether you itemize or take the standard deduction. These include contributions to traditional IRAs, student loan interest, and self-employment taxes. These deductions reduce your adjusted gross income (AGI), which can affect your eligibility for other tax benefits.

Tax credits are even more valuable than deductions because they reduce your tax liability dollar for dollar. Some common tax credits include the Child Tax Credit, which provides up to $2,000 per qualifying child; the Earned Income Tax Credit, which benefits low-to-moderate-income working individuals and families; education credits like the American Opportunity Tax Credit; and energy credits for making energy-efficient improvements to your home. Some credits are refundable, meaning you can receive the credit even if it exceeds your tax liability.

Filing Your Tax Return

Filing a tax return is an annual requirement for most Americans. The tax filing season typically runs from late January to mid-April, with the deadline usually falling on April 15. If the 15th falls on a weekend or holiday, the deadline is extended to the next business day. Taxpayers can request an automatic six-month extension to file, but this is an extension to file, not an extension to pay. Any taxes owed are still due by the original deadline.

There are several ways to file your tax return. Many people use tax preparation software, which guides you through the process and helps ensure accuracy. Popular options include TurboTax, H&R Block, and TaxAct. These programs are particularly helpful for people with relatively straightforward tax situations. For those with more complex situations, such as business owners or people with significant investment income, hiring a professional tax preparer or certified public accountant (CPA) may be worthwhile.

The IRS also offers Free File, a partnership with tax software companies that provides free tax preparation and filing services for taxpayers with adjusted gross incomes below a certain threshold. Additionally, the IRS Volunteer Income Tax Assistance (VITA) program offers free tax help to people who generally make $64,000 or less, persons with disabilities, and limited English-speaking taxpayers. The Tax Counseling for the Elderly (TCE) program offers free tax help for all taxpayers, particularly those who are 60 years of age and older.

When filing your tax return, you will need various documents, including W-2 forms from employers, 1099 forms for other types of income, records of deductible expenses, and documentation for any tax credits you plan to claim. Keeping good records throughout the year makes the filing process much easier and can help you in case of an audit.

After you file your return, the IRS will process it and either issue a refund if you overpaid your taxes or send a bill if you underpaid. Most refunds are issued within 21 days for electronically filed returns. You can check the status of your refund using the “Where’s My Refund?” tool on the IRS website.

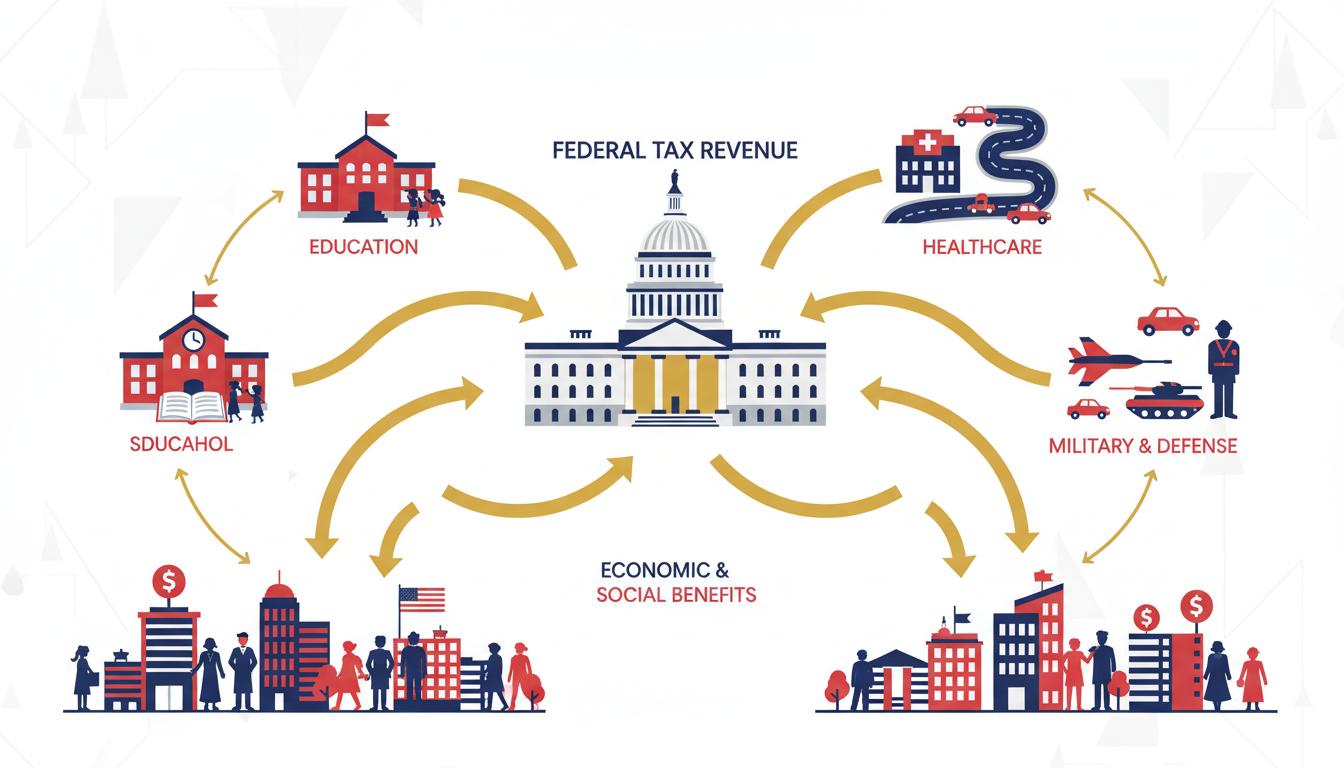

Where Your Tax Dollars Go

Understanding where your tax dollars go can help you appreciate the role taxes play in society. The federal government collects trillions of dollars in tax revenue each year, and this money funds a wide range of programs and services that affect the daily lives of all Americans.

Figure 2: Federal tax revenue flows to various essential government programs and services.

The largest portion of federal spending goes to mandatory programs, which are required by law and do not require annual approval by Congress. Social Security is the biggest mandatory program, providing retirement benefits to millions of Americans. Medicare and Medicaid, which provide health coverage for seniors, low-income individuals, and people with disabilities, are also major mandatory spending programs. Together, these three programs account for nearly half of all federal spending.

Defense spending is another major category of federal expenditure. This includes funding for the Department of Defense, military operations, weapons systems, and personnel costs. Defense spending typically accounts for about 15-20% of the federal budget, though this percentage has fluctuated over time based on geopolitical circumstances.

Interest on the national debt is another significant expense. When the government spends more than it collects in revenue, it must borrow money to make up the difference. The interest payments on this accumulated debt now total hundreds of billions of dollars each year. This is money that cannot be used for other programs and represents a cost that future generations will continue to bear.

Discretionary spending, which requires annual approval by Congress, funds most other federal programs. This category includes education, transportation, scientific research, environmental protection, international affairs, and the operation of federal agencies. While discretionary spending receives significant attention in budget debates, it actually represents a relatively small portion of total federal spending compared to mandatory programs.

At the state and local level, tax revenue primarily funds education, which is typically the largest expense for state and local governments. Other major categories include health and human services, transportation, public safety, and government administration. The specific allocation of funds varies significantly from one state or locality to another based on priorities and needs.

Tax Planning Strategies

Effective tax planning can help you minimize your tax liability and keep more of your hard-earned money. While tax evasion is illegal, tax avoidance through legitimate planning strategies is perfectly legal and smart financial management. Here are some strategies that can help you reduce your tax burden.

One of the most effective tax planning strategies is to maximize contributions to tax-advantaged retirement accounts. Contributions to traditional 401(k) plans and traditional IRAs are typically tax-deductible, reducing your taxable income in the current year. The money in these accounts grows tax-deferred until retirement, when you will likely be in a lower tax bracket. For 2026, the 401(k) contribution limit is expected to be around $23,500 for those under 50, with an additional catch-up contribution for those 50 and older.

Health Savings Accounts (HSAs) offer a triple tax advantage for those with high-deductible health plans. Contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are tax-free. Unlike Flexible Spending Accounts (FSAs), HSA balances roll over from year to year, making them a powerful long-term savings vehicle for healthcare expenses.

Timing your income and deductions can also be an effective strategy. If you have control over when you receive income or when you pay deductible expenses, you may be able to time these events to your tax advantage. For example, if you expect to be in a lower tax bracket next year, you might defer some income until then. Conversely, if you expect to be in a higher bracket next year, you might accelerate deductions into the current year.

Charitable giving can provide significant tax benefits. Cash donations to qualified charities are deductible if you itemize, and donations of appreciated securities can be particularly advantageous. When you donate appreciated stock or mutual funds that you have held for more than a year, you can deduct the full fair market value without paying capital gains tax on the appreciation.

Tax-loss harvesting is a strategy that involves selling investments at a loss to offset capital gains. If your capital losses exceed your capital gains, you can use up to $3,000 of the excess loss to offset ordinary income, with any remaining losses carried forward to future years. This strategy can be particularly useful in volatile markets.

For business owners and self-employed individuals, there are numerous tax planning opportunities. Deductible business expenses can include home office expenses, vehicle expenses, professional development costs, and health insurance premiums. Choosing the right business structure (sole proprietorship, partnership, LLC, S corporation, or C corporation) can also have significant tax implications.

Common Tax Mistakes to Avoid

Even honest taxpayers can make mistakes on their tax returns, and these errors can be costly. Some mistakes result in delayed refunds, while others can lead to penalties and interest charges. Here are some of the most common tax mistakes and how to avoid them.

One of the most common mistakes is choosing the wrong filing status. Your filing status (single, married filing jointly, married filing separately, head of household, or qualifying widow/widower) affects your tax bracket, your standard deduction, and your eligibility for certain credits. Choosing the wrong status can cost you thousands of dollars. For most married couples, filing jointly results in the lowest tax liability, but there are exceptions.

Math errors are another frequent problem. While tax software has reduced the incidence of calculation errors, mistakes can still occur when entering numbers. Double-check all entries, especially Social Security numbers, which are a common source of errors. An incorrect Social Security number can delay your refund and may even result in the IRS rejecting certain credits.

Many taxpayers fail to report all of their income. Remember that the IRS receives copies of all W-2s and 1099s issued to you, so they know how much income you should be reporting. Failing to report income can trigger an audit and result in penalties and interest. This includes not only wages and investment income but also income from side gigs, freelance work, and cryptocurrency transactions.

Missing deductions and credits is another costly mistake. Many taxpayers leave money on the table by not claiming credits and deductions they are entitled to. Common overlooked deductions include student loan interest, educator expenses, and state sales taxes. Frequently missed credits include the Saver’s Credit for retirement contributions and education credits.

Failing to sign and date your return is a surprisingly common error. An unsigned return is not valid, and the IRS will return it to you, delaying any refund you may be owed. If you are filing a joint return, both spouses must sign. When filing electronically, you will use a PIN or your prior-year adjusted gross income to sign your return.

Missing the filing deadline can result in penalties and interest. If you cannot file by the deadline, be sure to request an extension. However, remember that an extension to file is not an extension to pay. If you owe taxes, you should estimate the amount and pay it by the original deadline to avoid failure-to-pay penalties and interest.

Understanding how taxes work in the United States is an essential life skill that can help you make better financial decisions and avoid costly mistakes. While the tax system can seem complex and intimidating, breaking it down into its component parts makes it much more manageable. By understanding the different types of taxes, how tax brackets work, what deductions and credits are available, and where your tax dollars go, you can approach tax season with confidence.

Remember that tax laws change frequently, and what is true today may not be true next year. Staying informed about changes to the tax code and how they affect you is an ongoing responsibility. Resources like the IRS website, reputable tax publications, and qualified tax professionals can help you stay up to date.

Effective tax planning is not about finding loopholes or avoiding taxes illegally. It is about understanding the rules and using them to your advantage. By taking advantage of tax-advantaged accounts, timing your income and deductions strategically, and claiming all the credits and deductions you are entitled to, you can minimize your tax burden while remaining fully compliant with the law.

Finally, remember that taxes are not just a burden but also a contribution to the common good. The roads you drive on, the schools your children attend, the military that protects the nation, and the social safety net that helps those in need are all funded by tax dollars. Understanding how taxes work helps you be a more informed citizen and a more effective advocate for how your tax dollars are spent.

Whether you choose to prepare your own taxes using software or hire a professional, the knowledge you have gained from this guide will serve you well. Taxes may never be enjoyable, but with the right understanding and preparation, they do not have to be a source of stress and anxiety. Take control of your tax situation, plan ahead, and make the tax system work for you.

Understanding Capital Gains and Investment Taxes

Investment income is taxed differently than ordinary income, and understanding these differences is crucial for effective tax planning. Capital gains are the profits you make from selling investments such as stocks, bonds, real estate, or other assets. The tax rate you pay on capital gains depends on how long you held the asset before selling it.

Short-term capital gains apply to assets held for one year or less, and they are taxed at the same rates as ordinary income. This means they are subject to your marginal tax rate, which could be as high as 37%. Long-term capital gains, on the other hand, apply to assets held for more than one year and benefit from preferential tax rates. For 2026, the long-term capital gains rates are expected to be 0% for taxpayers in the 10% and 12% brackets, 15% for most other taxpayers, and 20% for high-income earners.

Qualified dividends, which are dividends paid by U.S. corporations and certain qualified foreign corporations, are also taxed at the preferential long-term capital gains rates. Non-qualified dividends are taxed as ordinary income. To be considered qualified, dividends must meet specific holding period requirements, generally more than 60 days during the 121-day period beginning 60 days before the ex-dividend date.

The Net Investment Income Tax (NIIT) is an additional 3.8% tax that applies to investment income for high-income taxpayers. This tax applies to individuals with modified adjusted gross income above $200,000 for single filers or $250,000 for married couples filing jointly. The NIIT applies to interest, dividends, capital gains, rental income, royalty income, and passive business income.

Self-Employment and Small Business Taxes

Self-employed individuals and small business owners face unique tax challenges and opportunities. Unlike employees who have taxes withheld from their paychecks, self-employed individuals must calculate and pay their own taxes, typically through quarterly estimated tax payments. They are responsible for both income tax and self-employment tax, which covers Social Security and Medicare contributions.

Self-employment tax is calculated on net earnings from self-employment, which is generally your business income minus business expenses. The self-employment tax rate is 15.3%, consisting of 12.4% for Social Security and 2.9% for Medicare. However, you can deduct the employer portion of self-employment tax when calculating your adjusted gross income, which provides some relief.

Business expenses are generally deductible if they are both ordinary and necessary for your business. Common deductible expenses include office supplies, professional development, business travel, meals (subject to limitations), home office expenses, and vehicle expenses. Keeping detailed records of all business expenses is essential for maximizing your deductions and supporting your claims in case of an audit.

The Qualified Business Income (QBI) deduction, also known as the Section 199A deduction, allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income. This deduction is available to owners of pass-through entities, including sole proprietorships, partnerships, S corporations, and limited liability companies (LLCs). There are income limitations and other restrictions, so consult a tax professional to determine your eligibility.

Estate and Gift Taxes

Estate and gift taxes apply to the transfer of wealth, either during life (gifts) or at death (estates). The federal estate tax applies to estates above a certain threshold, which is expected to be around $13.9 million per individual for 2026. This means that only a small percentage of estates are subject to federal estate tax. Married couples can combine their exemptions, effectively doubling the amount they can pass to heirs tax-free.

The estate tax rate is 40% on the value of the estate above the exemption amount. However, there are numerous strategies for reducing estate tax liability, including annual gift exclusions, charitable giving, and the use of trusts. The annual gift exclusion allows you to give up to $18,000 per recipient in 2026 without using any of your lifetime estate and gift tax exemption. Married couples can combine their exclusions to give up to $36,000 per recipient.

Gift taxes are generally paid by the donor, not the recipient. However, most gifts are not subject to gift tax due to the annual exclusion and the lifetime exemption. Gifts that exceed the annual exclusion count against your lifetime exemption, reducing the amount you can transfer at death without estate tax. Medical and educational expenses paid directly to institutions on behalf of someone else are not considered gifts for tax purposes.

Tax Audits and Your Rights as a Taxpayer

The thought of a tax audit can be intimidating, but understanding the process and your rights can help alleviate anxiety. The IRS conducts audits to verify that taxpayers have reported their income correctly and claimed only the deductions and credits to which they are entitled. Most audits are conducted by mail and involve specific issues rather than a comprehensive examination of your entire return.

The IRS uses various methods to select returns for audit, including computer scoring systems that identify returns with unusual patterns, information matching (comparing reported income to information documents), and related examinations (audits of business partners or investors). Being selected for an audit does not necessarily mean you have done anything wrong.

As a taxpayer, you have important rights during the audit process. These include the right to professional and courteous treatment by IRS employees, the right to privacy and confidentiality, the right to know why the IRS is asking for information and how it will be used, the right to representation by yourself or an authorized representative, and the right to appeal disagreements. The Taxpayer Bill of Rights outlines these protections in detail.

If you disagree with the outcome of an audit, you have several options. You can request a conference with an IRS manager, file an appeal with the IRS Office of Appeals, or in some cases, take your case to tax court. It is often advisable to consult with a tax professional if you are facing an audit or disagree with the IRS findings.

The Future of Taxation in America

The tax landscape in the United States is constantly evolving, with changes in tax laws, rates, and policies occurring regularly. Understanding potential future trends can help you plan more effectively for your financial future. Tax reform has been a recurring theme in American politics, with significant changes enacted in recent years and more likely to come.

One area of ongoing debate is the progressivity of the tax system. Some policymakers advocate for higher taxes on wealthy individuals and corporations to fund social programs and reduce income inequality. Others argue for lower tax rates to stimulate economic growth and investment. These debates will continue to shape tax policy in the coming years.

Technology is also changing how taxes are administered and collected. The IRS has been investing in modernizing its systems, making it easier for taxpayers to file electronically, check refund status, and communicate with the agency. Digital currencies and the gig economy present new challenges for tax collection, and the IRS is working to adapt its enforcement strategies accordingly.

International tax issues are becoming increasingly important in our globalized economy. The United States taxes its citizens on worldwide income, regardless of where they live, which is unusual among developed countries. This creates complexity for Americans living abroad and for multinational corporations. International agreements and tax treaties attempt to address some of these issues, but challenges remain.

Staying informed about changes in tax law and planning accordingly is essential for minimizing your tax burden and avoiding surprises. Working with qualified tax professionals, staying current on tax news, and being proactive in your tax planning can help you navigate the ever-changing tax landscape successfully.