America has long been known as the land of opportunity, a place where anyone willing to work hard could build a better life for themselves and their families. For generations, this promise held true. The middle class grew, prosperity was shared broadly, and the American Dream seemed within reach for millions of people. But somewhere along the way, something fundamental changed in how wealth is created, distributed, and preserved in this country.

Today, the United States faces a crisis of inequality that threatens the very fabric of our society. The gap between the rich and everyone else has grown to levels not seen since the Gilded Age of the 1920s. The wealthiest Americans have accumulated fortunes that would have been unimaginable just a few decades ago, while ordinary working families struggle to keep up with rising costs of housing, healthcare, and education. This is not merely an economic issue; it is a moral challenge that calls into question who we are as a nation and what kind of future we want to build.

The statistics are staggering and paint a picture of a deeply divided nation. According to the latest data from the Federal Reserve, the top 1% of American households now own 31.7% of all wealth in the United States, a record high since tracking began in 1989. Meanwhile, the bottom 50% of households collectively hold just 2.5% of the nation’s wealth. To put this in perspective, the wealthiest 1% control more wealth than the entire bottom 90% combined.

This article examines the growing wealth gap in America from multiple angles. We will explore the historical forces that shaped our current economic landscape, analyze the data behind today’s inequality, investigate the root causes driving this divide, and consider what can be done to create a more equitable society. The goal is not simply to document a problem but to understand it deeply enough that meaningful solutions become possible.

The Post-War Boom Years

To understand where we are today, we must first look back at where we came from. The period from the end of World War II through the early 1970s is often remembered as a golden age of American prosperity. During these decades, the United States experienced unprecedented economic growth, and crucially, that growth was widely shared across the income spectrum.

In the years following World War II, American workers experienced rising wages that kept pace with productivity gains. As companies became more efficient and profitable, those gains translated into higher paychecks for employees. The result was a thriving middle class that could afford homes, cars, college educations, and family vacations. A single income was often enough to support a comfortable lifestyle, and economic mobility was a realistic possibility for millions of families.

Several factors contributed to this era of shared prosperity. Strong labor unions gave workers collective bargaining power to negotiate fair wages and benefits. Progressive tax policies ensured that the wealthy paid their fair share, funding public investments in infrastructure, education, and research. The GI Bill helped millions of returning veterans attend college and buy homes, creating pathways to the middle class. And regulations on the financial sector prevented the kind of risky behavior that could destabilize the economy.

During this period, the Gini coefficient, a measure of income inequality where 0 represents perfect equality and 1 represents perfect inequality, remained relatively stable. In 1947, the Gini coefficient for family income was approximately 0.376. By 1968, it had actually declined to around 0.348, indicating that incomes were becoming more equal, not less. This was a remarkable achievement for a growing economy and demonstrated that prosperity and equality were not mutually exclusive.

The Turning Point: 1970s and Beyond

The 1970s marked a significant turning point in American economic history. A series of shocks, including the oil crisis, stagflation, and increased global competition, challenged the post-war economic model. But policy responses to these challenges fundamentally altered the trajectory of wealth distribution in America.

Beginning in the late 1970s and accelerating through the 1980s, a new economic philosophy gained prominence. This approach emphasized deregulation, tax cuts for the wealthy and corporations, free trade, and reduced government intervention in the economy. While these policies contributed to overall economic growth, they also fundamentally changed how the benefits of that growth were distributed.

The Tax Reform Act of 1986 lowered the top marginal income tax rate from 50% to 28%, one of the most significant tax cuts for high earners in American history. While proponents argued that these cuts would spur investment and growth that would benefit everyone, the reality proved more complicated. The wealthy did see substantial gains, but wages for ordinary workers stagnated even as productivity continued to rise.

The decline of labor unions also accelerated during this period. In the 1950s, approximately one-third of American workers belonged to a union. By 2022, that figure had fallen to just 10.1%. As union membership declined, so did workers’ bargaining power. Wage growth slowed, benefits became less generous, and job security diminished. The link between productivity and wages that had characterized the post-war era was effectively broken.

From 1979 to 2024, average hourly compensation increased just 29.4% after adjusting for inflation, while worker productivity increased 80.9%. In other words, productivity grew at a rate 2.7 times as fast as worker pay. The gap between what workers produced and what they were paid flowed primarily to shareholders, executives, and owners of capital.

Current State of Wealth Inequality in America

The Top 1% vs. The Bottom 50%

The numbers describing today’s wealth inequality are difficult to comprehend. They speak to a level of economic concentration that challenges our fundamental understanding of fairness and opportunity in America. Let us examine what the data tells us about who owns what in the United States today.

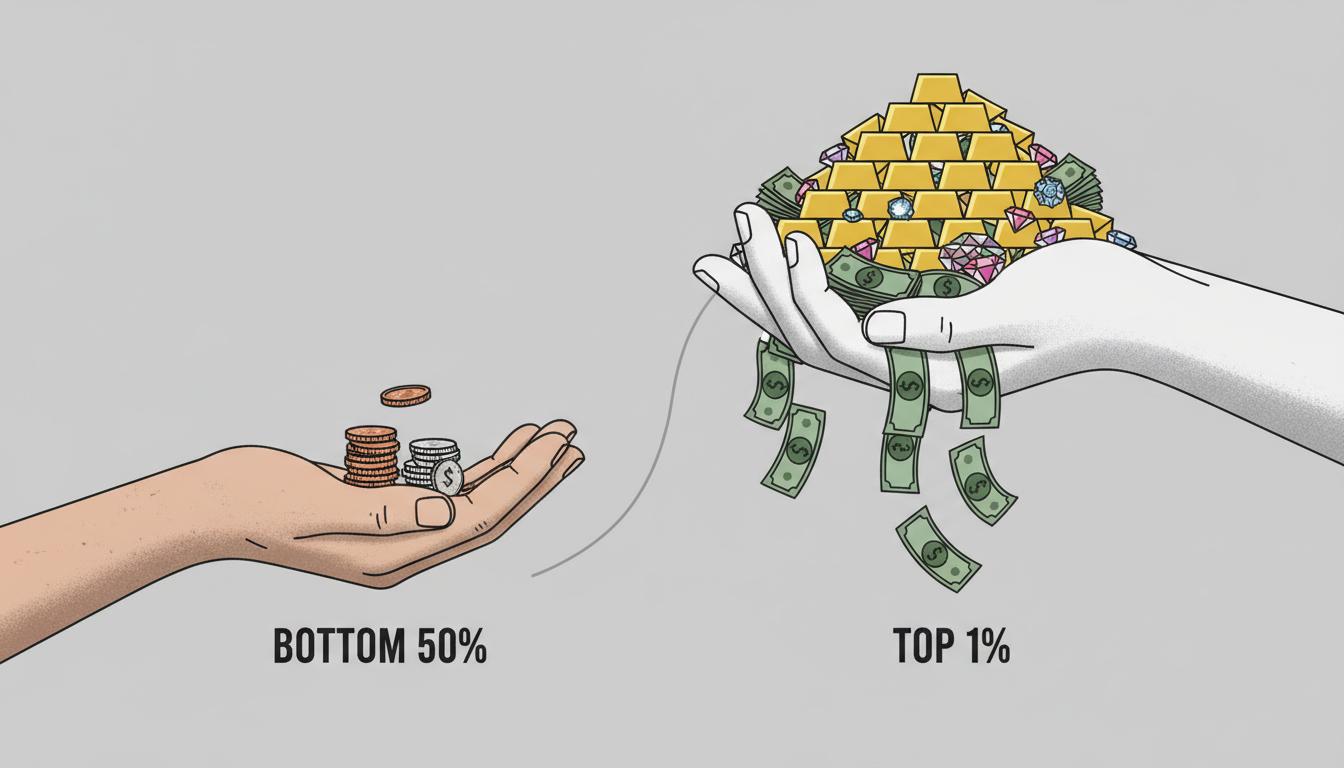

As of the third quarter of 2025, the top 1% of American households owned 31.7% of all U.S. wealth, the highest share on record since the Federal Reserve began tracking household wealth in 1989. This represents approximately $55 trillion in assets held by just over 1.3 million households. To put this in context, the wealth held by this small group is roughly equal to the combined wealth of the bottom 90% of Americans.

The concentration becomes even more extreme when we look at the very top of the distribution. The top 0.1% of households, about 130,000 families, hold approximately 13.9% of all wealth. These are the billionaires and centi-millionaires whose fortunes have grown exponentially in recent decades. In 1989, there were 66 billionaires in the United States. By September 2025, there were 905 billionaires with a combined wealth of $7.8 trillion.

At the other end of the spectrum, the picture is equally striking but for opposite reasons. The bottom 50% of American households collectively own just 2.5% of the nation’s wealth. Their average net worth is approximately $60,000, and many of these households have zero or even negative wealth, meaning the value of their debts exceeds the value of their assets. An estimated 28% of Black households and 26% of Latino households had zero or negative wealth in 2019, twice the level of white households.

The contrast between how the wealthy and ordinary Americans build wealth is also revealing. For the top 1%, more than half of their wealth comes from stocks, mutual funds, and other financial assets. These investments have delivered extraordinary returns in recent decades, particularly after the 2008 financial crisis as central banks kept interest rates low and stock markets soared. Meanwhile, for the bottom 90%, the majority of wealth comes from their homes. When the housing market collapsed in 2008, these families suffered devastating losses from which many have never fully recovered.

Figure 1: The stark divide between America’s wealthy elite and working-class families

The Racial Wealth Divide

Wealth inequality in America cannot be understood without examining its racial dimensions. The legacy of slavery, segregation, and discriminatory policies has created a racial wealth gap that persists and, in some ways, has widened over time. This is not a matter of individual choices or cultural differences but of systemic barriers that have prevented Black, Latino, and other minority families from building and transferring wealth across generations.

According to Federal Reserve data, white households held 84.2% of all U.S. wealth as of the fourth quarter of 2023, while making up only 66% of households. By contrast, Black families accounted for 11.4% of households but owned just 3.4% of total family wealth. Hispanic families represented 9.6% of households and owned 2.3% of total family wealth. These disparities are not accidental but the result of centuries of policies that favored white families while excluding or disadvantaging families of color.

The median Black family has a net worth of $44,100, just 15.5% of the $282,310 median white wealth. The typical Latino family, with $62,120, owns just 21.8% of the wealth of the median white family. These gaps have narrowed only slightly since 1989, despite significant progress in other areas of racial equality. Wealth, it seems, is stickier than income, and historical disadvantages compound over time.

Homeownership is one of the primary ways American families build wealth, and here the racial disparities are particularly stark. Between 1960 and 2020, the rate of Black homeownership increased, but the gap in ownership rates between Black and white families actually widened from 26 percentage points to 30 percentage points. Structural barriers, including lower incomes, higher rates of mortgage denials, and continued residential segregation, deny many Black families the opportunity to acquire this wealth-building asset.

The consequences of the racial wealth gap extend far beyond individual families. Communities with less wealth have fewer resources for schools, infrastructure, and local businesses. Children grow up with fewer opportunities, perpetuating intergenerational cycles of disadvantage. And the loss of human potential affects not just those communities but the entire nation.

Generational Wealth Disparities

The wealth gap also has a significant generational dimension. Younger Americans today face economic challenges that their parents and grandparents did not encounter at the same age. From student debt to housing costs to job insecurity, millennials and Gen Zers are building wealth more slowly than previous generations did.

However, recent data from the Federal Reserve offers a surprising finding. When comparing generations at the same age, younger Americans (millennials and Gen Zers) actually own $1.23 for every $1 of wealth owned by Gen Xers at the same age, and $1.35 for every $1 of wealth owned by baby boomers at the same age. This reflects historically high wealth levels following the COVID-19 pandemic, including increased savings and rising home values.

Yet this aggregate picture masks significant disparities within younger generations. While some young people, particularly those from wealthy families, have benefited from parental support and rising asset values, many others remain burdened by student debt, high rent, and stagnant wages. The wealth gap within younger generations may be as significant as the gap between generations.

Education has become an increasingly important determinant of wealth. Households headed by someone with a four-year college degree have substantially more wealth than those without. Those with some college education but no degree have just 30 cents for every $1 of wealth held by college graduates. Those with only a high school diploma have 22 cents, and those without a high school diploma have just 9 cents. As the returns to education have increased, so have the consequences of not having access to it.

Root Causes of the Growing Wealth Gap

Policy Choices and Tax Reform

The wealth gap did not emerge by accident. It is the result of policy choices made over decades that have systematically favored the wealthy while undermining the economic security of working families. Understanding these choices is essential to understanding how we arrived at our current situation and what might be done to change course.

Tax policy has played a particularly important role. Over the past several decades, tax rates on the wealthy have declined significantly. The top marginal income tax rate was 91% in the 1950s and 70% in the 1970s. Today, it stands at 37%. Capital gains, which make up a substantial portion of income for the wealthy, are taxed at even lower rates, with a maximum rate of 20%. These preferential rates for investment income mean that wealthy individuals often pay lower effective tax rates than middle-class workers.

The estate tax, which was designed to prevent the accumulation of dynastic wealth, has been weakened repeatedly. The exemption amount has been raised substantially, and the rate has been lowered. As a result, very few estates now pay any tax at all. This allows wealthy families to pass fortunes to their children and grandchildren with minimal taxation, perpetuating inequality across generations.

Corporate tax policy has also contributed to inequality. The corporate tax rate has been reduced from 35% to 21%, and various loopholes allow many profitable corporations to pay little or no tax. Stock buybacks, which primarily benefit wealthy shareholders, have exploded in recent years. Meanwhile, wages for workers have stagnated even as corporate profits have reached record highs.

The Decline of Labor Unions

The decline of organized labor is one of the most significant developments in American economic life over the past half-century. Unions gave workers collective power to negotiate better wages, benefits, and working conditions. As union membership has fallen, so has workers’ ability to capture a fair share of the wealth they create.

In the 1950s and 1960s, approximately one-third of American workers belonged to a union. Today, that figure has fallen to just over 10%. The decline has been particularly sharp in the private sector, where only 6% of workers are now unionized. This decline was not inevitable but resulted from policy choices, including so-called “right-to-work” laws, weak enforcement of labor protections, and employer opposition to organizing.

The consequences of deunionization are clear in the data. Union workers earn significantly more than their non-union counterparts, with the gap particularly wide for women and workers of color. In 2024, median weekly wages for full-time unionized women amounted to $1,232, $216 more than non-unionized women’s earnings. Unions also help reduce wage inequality within firms and across the economy.

Beyond wages, unions have historically played a crucial role in advocating for policies that benefit all workers, not just their members. The weekend, the eight-hour workday, workplace safety regulations, and Social Security were all advanced by the labor movement. As unions have weakened, so has the political voice of working people.

Education and Opportunity Gaps

Education has always been a key pathway to economic opportunity in America. But access to quality education has become increasingly unequal, with profound implications for wealth accumulation. The cost of higher education has skyrocketed, while public investment in schools has become more unequal across districts.

Student debt has become a crushing burden for millions of young Americans. Total student loan debt now exceeds $1.7 trillion, more than credit card debt or auto loan debt. For many graduates, monthly loan payments consume a significant portion of their income, making it difficult to save for a home, start a business, or invest for retirement. The burden falls disproportionately on Black students, who are more likely to borrow and borrow more.

K-12 education funding remains heavily dependent on local property taxes, meaning that wealthy communities can spend far more per student than poor communities. This creates a self-perpetuating cycle where children in wealthy areas receive better educations, leading to better opportunities, while children in poor areas fall further behind. The result is less economic mobility and more inequality.

Figure 2: The dramatic difference in wealth held by the top 1% versus the bottom 50%

Consequences of Extreme Inequality

Extreme wealth inequality is not merely an abstract economic concern. It has real consequences for individuals, communities, and the nation as a whole. Understanding these consequences helps explain why addressing inequality should be a priority for policymakers and citizens alike.

Perhaps the most fundamental consequence is reduced economic mobility. The American Dream of rising from poverty to prosperity becomes harder to achieve when the rungs on the economic ladder are so far apart. Children born into wealthy families have access to better schools, safer neighborhoods, professional networks, and financial support that give them enormous advantages. Children born into poor families face obstacles at every turn. Research shows that economic mobility has declined in the United States over recent decades, meaning that where you start in life increasingly determines where you end up.

Inequality also has significant health consequences. Studies consistently show that more unequal societies have worse health outcomes, even for the wealthy. Chronic stress from financial insecurity contributes to a range of health problems, from heart disease to depression. Life expectancy in the United States has actually declined in recent years, a shocking development for a wealthy nation, and inequality is a significant contributing factor.

The political consequences of inequality are equally concerning. Wealth translates into political power, and as wealth concentrates, so does influence over the political process. The wealthy can afford to make campaign contributions, hire lobbyists, and fund think tanks that shape policy debates. The result is a political system that responds more to the preferences of the rich than to the needs of ordinary citizens. This undermines the democratic principle of political equality and can lead to policies that further exacerbate economic inequality.

Extreme inequality also threatens economic stability. When wealth concentrates at the top, consumer demand can weaken because wealthy individuals spend a smaller share of their income than middle-class and poor families. This can lead to slower economic growth and more frequent financial crises. The Great Depression and the 2008 financial crisis were both preceded by periods of rising inequality, and economists have identified inequality as a contributing factor to both.

Social cohesion also suffers in highly unequal societies. When the gap between rich and poor becomes too wide, trust breaks down, social divisions deepen, and the sense of shared national purpose weakens. This can manifest in increased crime, political polarization, and social unrest. The challenges facing American democracy today cannot be separated from the economic inequality that has grown over recent decades.

The Path Forward: Potential Solutions

Addressing the wealth gap will require sustained effort across multiple fronts. There is no single solution that will solve the problem overnight. But a combination of policy reforms could begin to reverse the trends of recent decades and create an economy that works for everyone, not just the wealthy few.

Tax reform is an essential component of any serious effort to reduce inequality. This includes raising tax rates on high incomes, treating capital gains more like ordinary income, strengthening the estate tax, and cracking down on tax avoidance by corporations and wealthy individuals. The revenue generated could fund investments in education, infrastructure, and social programs that benefit all Americans.

Strengthening workers’ rights and bargaining power is equally important. This means making it easier for workers to organize unions, enforcing labor laws more effectively, and raising the minimum wage to a living wage. The federal minimum wage has been stuck at $7.25 per hour since 2009, and the tipped minimum wage for restaurant servers has been frozen at $2.13 per hour since 1991. Raising these wages would directly benefit millions of working families.

Investing in education at all levels is crucial for expanding opportunity. This includes increasing funding for public schools in low-income areas, making community college and public universities tuition-free, and addressing the student debt crisis. Education is not a panacea, but it remains one of the most important tools for economic mobility.

Addressing the racial wealth gap requires targeted policies that acknowledge the historical disadvantages faced by Black and Latino communities. This includes measures to increase homeownership, support minority-owned businesses, and ensure fair access to credit and capital. Baby bonds, which would provide every child with a nest egg at birth that grows over time, could help reduce the intergenerational transmission of wealth inequality.

Healthcare reform is also essential. Medical debt is a leading cause of bankruptcy in the United States, and lack of access to affordable healthcare can devastate family finances. Universal healthcare coverage would not only improve health outcomes but also provide economic security for millions of families.

Finally, political reform is necessary to ensure that the voices of ordinary citizens are heard in the political process. This includes campaign finance reform, limits on lobbying, and measures to increase voter participation. Without political reform, it will be difficult to achieve the other reforms needed to address economic inequality.

Conclusion

The growing wealth gap in the United States represents one of the defining challenges of our time. It threatens our economy, undermines our democracy, and calls into question our nation’s commitment to opportunity and fairness. The statistics are stark: the top 1% control nearly a third of all wealth, while the bottom half own just 2.5%. These numbers reflect decades of policy choices that have favored the wealthy at the expense of working families.

But history shows that inequality is not inevitable. The post-war period demonstrated that prosperity can be widely shared. Other wealthy nations have maintained lower levels of inequality while achieving comparable or better economic outcomes. The question is not whether we can afford to address inequality but whether we can afford not to.

Addressing the wealth gap will require political will and sustained effort. It will mean making different choices about taxation, labor policy, education, and social investment. It will require us to recognize that we are all in this together and that the health of our society depends on the well-being of all its members, not just the wealthy few.

The American Dream has always been about more than just getting rich. It is about the promise that anyone willing to work hard can build a decent life for themselves and their families. It is about the belief that we are a nation of equals, where birth does not determine destiny. Restoring that promise will not be easy, but it is essential if we are to remain a nation worthy of our highest ideals.

The wealth gap is not just an economic problem; it is a moral challenge. How we respond to it will define what kind of country we are and what kind of future we will leave to our children. The time for action is now.

Global Context: How the U.S. Compares

When we look beyond America’s borders, we find that wealth inequality is a global phenomenon, but the United States stands out among wealthy nations for the extent of its inequality. According to data from the Organisation for Economic Co-operation and Development (OECD), the United States has higher levels of income inequality than most other developed countries, including Germany, France, Japan, and Canada.

The Gini coefficient provides a useful point of comparison. As of 2023, the United States had a Gini coefficient of approximately 41.8, higher than most European nations. For comparison, Germany’s Gini coefficient is around 31, and Denmark’s is approximately 27. These differences reflect different policy choices about taxation, social welfare, and labor market regulation. Countries with stronger social safety nets, more progressive tax systems, and stronger labor protections tend to have lower levels of inequality.

What makes the American case particularly striking is that extreme inequality coexists with great abundance. The United States remains one of the wealthiest countries in the world, with a GDP per capita that ranks among the highest globally. The problem is not a lack of wealth but how that wealth is distributed. This makes American inequality a matter of choice rather than necessity.

International comparisons also reveal that high inequality is not a prerequisite for economic success. Countries with lower inequality often match or exceed the United States on measures of economic growth, innovation, and living standards. The Nordic countries, for example, combine relatively low inequality with high levels of prosperity, suggesting that fairness and economic success can go hand in hand.

The Role of Technology and Automation

Technological change has been a major driver of economic transformation in recent decades, and its impact on inequality has been profound. Automation and artificial intelligence have eliminated many middle-skill jobs while creating new opportunities at the high end of the skill distribution. This has contributed to what economists call “job polarization,” with growth at the top and bottom of the wage distribution but contraction in the middle.

The benefits of technological progress have flowed disproportionately to those who own and develop technology. The founders, early employees, and investors in successful technology companies have accumulated enormous fortunes. Meanwhile, workers whose jobs have been automated or outsourced have seen their livelihoods disappear or their wages stagnate.

The platform economy has created new forms of work that offer flexibility but often lack the protections and benefits of traditional employment. Gig workers are classified as independent contractors rather than employees, which means they are not entitled to minimum wage, overtime pay, unemployment insurance, or workers’ compensation. This has created a new class of workers who bear the risks of employment without the traditional protections.

Addressing the challenges posed by technological change will require new approaches to education and training, social insurance, and labor market regulation. Lifelong learning must become a reality, not just a slogan, with public investment in training programs that help workers adapt to changing economic conditions. Portable benefits that follow workers from job to job could provide security in an increasingly fluid labor market.

Housing and the Wealth Gap

Housing plays a central role in the wealth gap story. For most American families, their home is their most valuable asset. The value of real estate owned by households exceeds $40 trillion, making it one of the largest components of household wealth. But access to homeownership has become increasingly unequal, with profound implications for wealth accumulation.

Home prices have risen much faster than wages in many parts of the country, putting homeownership out of reach for many young people and working families. In desirable urban areas, the cost of housing has skyrocketed, creating what some economists call a “housing affordability crisis.” Those who already own homes have seen their wealth increase, while renters fall further behind.

The 2008 financial crisis demonstrated both the importance of housing wealth and its vulnerability. When the housing bubble burst, millions of families lost their homes to foreclosure, and housing wealth evaporated. The recovery was uneven, with some areas bouncing back quickly while others continue to struggle. Black and Latino communities, which were disproportionately targeted for subprime loans, suffered particularly severe losses.

Addressing the housing dimension of wealth inequality will require a multi-faceted approach. This includes increasing the supply of affordable housing, reforming zoning laws that restrict development, providing down payment assistance for first-time homebuyers, and strengthening protections against predatory lending and housing discrimination.

The Psychological Toll of Economic Insecurity

The wealth gap is not just about numbers on a spreadsheet; it has profound psychological and social consequences. Living with economic insecurity takes a toll on mental and physical health. Chronic stress from worrying about paying bills, keeping a roof overhead, and providing for children can lead to anxiety, depression, and a host of stress-related health problems.

Research has shown that economic inequality affects not just the poor but society as a whole. In more unequal societies, people report lower levels of trust, higher levels of anxiety, and poorer health outcomes across the income spectrum. The constant comparison with those who have more, amplified by social media and advertising, can lead to feelings of inadequacy and resentment.

Children growing up in poverty face particular challenges. The stress of economic insecurity can impair cognitive development, affect school performance, and limit future opportunities. The effects of childhood poverty can persist throughout life, perpetuating intergenerational cycles of disadvantage.

Addressing the psychological dimensions of inequality requires not just economic reforms but also a cultural shift in how we think about success, worth, and the good life. We need to recognize that human dignity does not depend on wealth and that everyone deserves respect regardless of their economic circumstances.