Walk into any grocery store in America today, and you will feel it immediately. The same cart of food that cost eighty dollars last year now costs a hundred. Fill up your car, and the pump seems to drain your wallet faster than ever. Pay the rent, and you wonder where all your money went. This is inflation, and it is hitting American families harder than they have been hit in decades.

But here is the uncomfortable truth that politicians and economists rarely discuss: inflation does not hurt everyone equally. While some Americans barely notice the rising prices, others are forced to choose between medicine and groceries. While wealthy investors find new ways to protect their money, working families watch their savings disappear. Inflation in America is not just an economic problem. It is a story about who has power, who has protection, and who gets left behind.

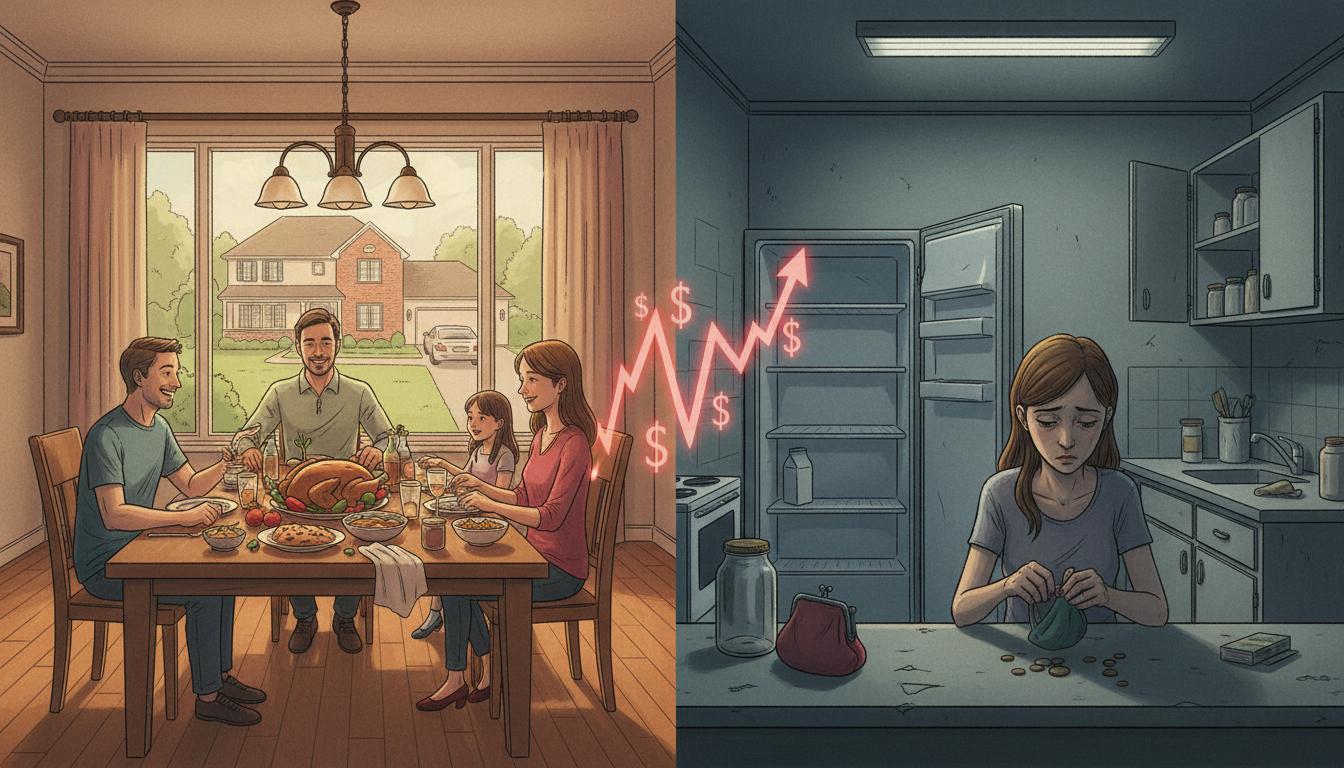

American families face difficult choices as grocery prices continue to climb.

Before we explore who suffers most, let us understand what inflation actually means. Simply put, inflation is when prices rise across the economy, and each dollar buys less than it did before. A candy bar that cost one dollar last year might cost a dollar ten this year. That ten-cent increase might seem small, but when it happens to everything you buy, the impact becomes enormous.

The United States has experienced several waves of inflation throughout its history, but the current situation feels different. After decades of relatively stable prices, Americans are now facing increases that affect nearly every aspect of daily life. Housing costs have skyrocketed. Healthcare expenses continue their relentless climb. Energy prices swing wildly. Even basic necessities like eggs, milk, and bread have become significantly more expensive.

Economists measure inflation using various indexes, with the Consumer Price Index being the most commonly cited. This index tracks the prices of a basket of goods and services that typical households purchase. When the index rises, it means the cost of living is going up. For most of 2022 and 2023, this index showed increases that Americans had not seen since the 1980s, creating genuine financial stress for millions ofpeople.

If you want to understand who really suffers from inflation in America, start with the working class. These are the people who get up every morning, go to jobs that keep society running, and still struggle to make ends meet. They are the cashiers, the delivery drivers, the factory workers, the nursing assistants, and the restaurant staff. They work hard, often holding down multiple jobs, but they live paycheck to paycheck with little room for error.

For these Americans, inflation is not an abstract economic concept. It is a daily crisis. When gas prices jump fifty cents per gallon, they must decide whether to drive to work or put food on the table. When rent increases by two hundred dollars, they face the terrifying prospect of eviction. When the price of ground beef goes up, they skip meals so their children can eat.

The cruel mathematics of inflation hits hardest at the bottom of the income ladder. A family earning thirty thousand dollars a year spends nearly all of their income on necessities. When those necessities become ten percent more expensive, they have no choice but to cut back somewhere. They cannot invest in stocks to hedge against inflation. They cannot negotiate a raise with their employer. They cannot move to a cheaper city because they cannot afford to relocate. They are trapped, and inflation is the walls closing in.

Consider Maria, a single mother working two jobs in Texas. She earns forty-five thousand dollars a year, which sounds decent until you factor in childcare, rent, utilities, and food. Before inflation surged, she managed to save a small amount each month. Now, with grocery bills up twenty percent and gas prices volatile, her savings have vanished. She has started visiting food banks, something she never imagined she would need to do. Maria’s story is not unique. It is being repeated in millions of American households.

The American middle class has long been considered the backbone of the nation, but inflation is threatening to break that backbone. These are the teachers, nurses, office workers, and small business owners who earn enough to live comfortably but not enough to be truly secure. They followed the rules, got educations, worked steadily, and expected to build better lives for their children.

For the middle class, inflation represents a slow erosion of everything they have worked for. The home they hoped to buy is now out of reach as mortgage rates have doubled. The college fund they have been building for their children buys less education each year. The retirement account that seemed adequate now looks frighteningly small.

The psychological impact on the middle class cannot be overstated. These are people who did everything right according to the American playbook, yet they feel themselves sliding backward. They watch their purchasing power decline while their salaries stay flat. They see their dreams of homeownership fade as housing prices climb faster than their savings. They worry that their children will not have the same opportunities they had.

Take David and Sarah, a married couple in their thirties living in Ohio. Both have college degrees and professional jobs. Together, they earn one hundred twenty thousand dollars a year, which would have been a comfortable income just a few years ago. But with childcare costing two thousand dollars a month, student loan payments of eight hundred dollars, and a mortgage that keeps rising due to property tax increases, they feel squeezed from every direction. They have postponed having a second child because they cannot afford it. Their story illustrates how inflation is reshaping fundamental life decisions for middle-class Americans.

The divide between those who weather inflation and those who suffer from it grows ever wider.

Now let us look at the other side of the coin. While working families struggle to afford groceries, wealthy Americans have ways to protect themselves from inflation, and some even profit from it. This is the uncomfortable reality of economic inequality: the same force that devastates some people barely touches others.

Wealthy Americans own assets that tend to increase in value during inflationary periods. Real estate becomes more valuable. Stocks often rise as companies pass increased costs to consumers. Commodities like gold traditionally serve as inflation hedges. While the poor watch their purchasing power evaporate, the rich see their net worth grow.

Consider how inflation affects debt. If you owe money, inflation actually helps you because you repay loans with dollars that are worth less than when you borrowed them. Wealthy Americans often use debt strategically to acquire more assets. They borrow at fixed rates to buy properties or businesses, then watch inflation erode the real value of their debt while their assets appreciate. It is a wealth-building strategy that is completely unavailable to people living paycheck to paycheck.

The wealthy also have access to financial advisors, tax strategies, and investment opportunities that protect their money. They can diversify internationally, invest in inflation-protected securities, and structure their holdings to minimize tax impacts. When inflation hits, they have options. For everyone else, there are only constraints.

Among all the groups suffering from inflation, seniors living on fixed incomes face a particularly cruel situation. These are people who worked their entire lives, saved diligently, and expected to enjoy a comfortable retirement. Instead, they find themselves watching their fixed incomes buy less and less each month.

Social Security benefits do include cost-of-living adjustments, but these adjustments often lag behind actual price increases. A senior who receives fifteen hundred dollars a month in Social Security might see a fifty-dollar increase when prices have already risen by a hundred dollars. The gap between their income and their expenses widens relentlessly.

Healthcare costs hit seniors especially hard. Older Americans typically need more medical care, and healthcare inflation has consistently outpaced general inflation for decades. Prescription medications, doctor visits, and medical procedures consume an ever-larger share of their fixed budgets. Many seniors face impossible choices between taking their medications as prescribed and paying for food or utilities.

Robert, a seventy-year-old retired teacher in Florida, illustrates this struggle. His pension and Social Security provide thirty-six thousand dollars a year, which was adequate when he retired five years ago. But with his rent increasing eight percent annually and his medication costs rising even faster, he has been forced to make drastic cuts. He no longer drives except for essential trips. He has canceled his cable television. He eats simpler meals. Despite a lifetime of work and saving, inflation is making his retirement years stressful rather than peaceful.

For young adults just beginning their careers and families, inflation creates obstacles that previous generations did not face. They are trying to establish themselves in an economy where everything costs more, wages have not kept pace, and the traditional paths to prosperity seem blocked.

Housing is the most obvious challenge. Young Americans today face home prices that are dramatically higher than what their parents paid at the same age, even after adjusting for inflation. When they cannot afford to buy, they rent, but rents have also increased substantially. Many young adults find themselves spending forty or even fifty percent of their income on housing, leaving little for saving or investment.

Student loan debt compounds the problem. Young Americans carry unprecedented levels of education debt, often totaling tens or even hundreds of thousands of dollars. These monthly payments reduce their ability to save for homes, start businesses, or build emergency funds. When inflation strikes, they have no cushion to absorb the shock.

The long-term consequences for young Americans are troubling. Delayed homeownership means delayed wealth building. Postponed families mean different life trajectories. Reduced saving means less security in old age. Inflation is not just making life harder for young people today. It is potentially altering the course of their entire.

Where you live in America significantly affects how inflation impacts you. Rural and urban Americans face different challenges, and inflation amplifies these differences in important ways.

Rural Americans often live farther from stores and services, meaning they drive more and feel fuel price increases more acutely. They have fewer shopping options, so they cannot easily comparison shop for better prices. Many rural communities have lost local grocery stores, forcing residents to drive long distances for basic necessities. When gas prices spike, the cost of simply obtaining food becomes prohibitive.

Urban Americans face their own inflation challenges. Housing costs in cities have exploded, with rents and home prices reaching levels that would have seemed impossible a generation ago. Parking, transportation, and childcare all cost more in cities. While urban residents might have more shopping options, the baseline cost of living is so high that inflation hits hard.

The geographic dimension of inflation means that national statistics often obscure local realities. A national inflation rate of six percent might mean four percent in some areas and ten percent in others. National averages cannot capture the experience of a rural family watching their heating bills double or an urban family seeing their rent increase by five hundred dollars a month.

Understanding who suffers from inflation naturally leads to questions about solutions. While individual Americans cannot control macroeconomic forces, there are strategies that can help, and there are policy approaches that might make a difference.

For individuals, the most important step is recognizing that inflation requires different financial behavior. Cash savings lose value during inflationary periods, so keeping large amounts in low-interest accounts is costly. Investing in assets that historically keep pace with inflation, such as real estate or diversified stock portfolios, can help preserve purchasing power. Of course, this advice is most applicable to those who have savings to invest, highlighting again how inflation disproportionately harms those with the least.

Negotiating salaries becomes more important during inflationary periods. Workers who accept raises below the inflation rate are effectively taking pay cuts. While not everyone has the leverage to negotiate, those who do should be assertive about maintaining their real compensation.

At the policy level, the Federal Reserve raises interest rates to combat inflation, though this approach can trigger recessions that also hurt working families. Government assistance programs can be expanded to help those most affected. Price controls, while politically appealing, have historically created more problems than they solve. There are no easy answers, only trade-offs.

The Human Cost of Economic Policy

As we have seen, inflation in America is not an equal-opportunity crisis. It falls hardest on those least able to bear it. Working families cut meals. Seniors skip medications. Young adults postpone dreams. The wealthy adjust their portfolios. This disparity reveals something fundamental about how our economy functions and who it serves.

The story of inflation is ultimately a story about power. Those with money, assets, and financial knowledge have tools to protect themselves. Those without these resources have only their labor, their resilience, and their hope that things will get better. When prices rise, the gap between these groups widens, and the American dream of shared prosperity becomes harder to believe in.

Understanding who really suffers from inflation is not just an academic exercise. It is essential for creating policies that genuinely help those in need. If we recognize that inflation hurts working families most, we can design assistance programs that target them. If we understand that seniors on fixed incomes face unique challenges, we can adjust benefits accordingly. If we see that young Americans are starting behind, we can create programs to help them catch up.

America has faced inflation before and emerged from it. The question is not whether we will survive this period, but who will bear the costs of getting through it. If history is any guide, those costs will fall most heavily on those with the least power to avoid them. Recognizing this reality is the first step toward building a more equitable response.

The next time you hear about inflation on the news, remember Maria struggling to feed her children, Robert choosing between medicine and food, and David and Sarah postponing their family plans. Behind every economic statistic are real people making impossible choices. Inflation in America is not just about prices. It is about people, and some of those people are suffering more than others. Understanding this truth is essential if we hope to build an economy that works for everyone, not just those who can afford to weather the storm.